Best High-Yield Savings Accounts for the Self-Employed (2026)

The best high-yield savings accounts of 2026 pay up to 5.00% APY - over 10x the national average. See the top picks, plus a tax tip every self-employed earner should steal.

Krislyn ChanKrislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces.

Krislyn ChanKrislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces. Reviewed bya tax professionalThis content has been reviewed by an Enrolled Agent (EA) with the IRS — the highest credential awarded by the agency. Enrolled Agents are empowered to represent all taxpayers before the IRS, on all types of tax-related matters. Accountants who earn this certification have passed a comprehensive three-part exam on individual and business tax returns. To maintain EA status, they must stay up to date in the field by completing 72 hours of continuing education every three years.

Reviewed bya tax professionalThis content has been reviewed by an Enrolled Agent (EA) with the IRS — the highest credential awarded by the agency. Enrolled Agents are empowered to represent all taxpayers before the IRS, on all types of tax-related matters. Accountants who earn this certification have passed a comprehensive three-part exam on individual and business tax returns. To maintain EA status, they must stay up to date in the field by completing 72 hours of continuing education every three years. If you keep an emergency fund or set aside your taxes in a traditional savings account, you are likely earning around 0.40% - the FDIC national average. The best high-yield savings accounts (HYSAs) pay more than 10 times that, with the exact same federal insurance.

Below are the top accounts available right now, what to look for before you open one, and a tax tip that makes a HYSA especially powerful if you are self-employed: it can quietly earn you hundreds of dollars on money you are setting aside for the IRS anyway.

What is the best high-yield savings account right now?

As of June 2026, the best high-yield savings accounts pay between 3.8% and 5% APY, compared with a national savings average of about 0.40% according to the FDIC. That means a high-yield account earns you roughly 10 times more on the same balance. So, if you've been letting your money sit in a traditional savings account, it's time to get smarter and move that money around to reap the most benefits for you!

Here are the standouts as of June 2026:

Bank | APY (as of June 2026) | Monthly fee | Minimum to earn APY | Best for |

|---|---|---|---|---|

Varo | Up to 5.00% | $0 | Direct deposit; rate applies to first $5,000 | Highest headline rate on a small balance |

Axos Bank | Up to 4.21% | $0 | $0 | High rate with no balance cap |

CIT Bank (Platinum Savings) | 4.10% | $0 | $5,000 balance | Larger balances |

Vio Bank | 4.03% | $0 | $100 to open | Low opening minimum |

EverBank (Performance Savings) | 3.90% | $0 | $0 | No conditions or hoops |

American Express | 3.85% | $0 | $0 | Trusted brand, simple terms |

Marcus by Goldman Sachs | 3.40% | $0 | $0 | Clean app, easy transfers |

Ally Bank | 3.10% | $0 | $0 | Savings buckets for goal tracking |

Rates change frequently and are not guaranteed. Confirm the current APY on each bank's site before opening an account. Sources: NerdWallet, Bankrate, and CNBC Select, June 2026.

Keeper pro tip: A high APY is worthless if it comes with strings. Before you chase the top number, check whether the rate is capped at a low balance (like Varo's $5,000 ceiling) or requires a recurring direct deposit. For most people, a slightly lower rate with no conditions beats a headline rate you can't actually keep.

What is a high-yield savings account?

A high-yield savings account is a savings account - usually offered by an online bank - that pays a much higher interest rate than a traditional brick-and-mortar bank. Online banks have lower overhead, so they pass the savings on as higher APYs to customers.

The mechanics are identical to a regular savings account: your money stays liquid, you can withdraw it, and it's insured. The only difference is the rate. There's almost no reason to keep an emergency fund or a short-term savings goal in a traditional savings account earning 0.4% versus an HYA earning 4%.

How to choose a high-yield savings account

Obviously, you want to go with the highest APY you can get to reap the most financial benefit, but other than the obvious, there are a couple other factors to consider:

1. FDIC insurance. This is non-negotiable. Federal insurance protects up to $250,000 per depositor, per institution. Every bank in the table above is FDIC-insured. If an account isn't insured, walk away.

2. Fees. The best HYSAs charge no monthly maintenance fee. A $5 monthly fee erases the interest on a few thousand dollars.

3. Minimums. Look at two numbers: the minimum to open and the minimum to earn the advertised rate. Some accounts pay the top APY only above a balance threshold (CIT requires $5,000 for 4.10%).

4. Access and transfer speed. How fast can you move money in and out? If you're using the account for quarterly tax payments (more on that below) you want transfers that clear in 1–2 business days.

Tax tips most self-employed people miss

Most people talk about stashing your emergency fund in a HYSA, but for self-employed people, there's more than just an emergency fund to think about.

If you're a freelancer, 1099 contractor, or small business owner, no one is withholding taxes from your income like with W-2 income. When that self-employment income hits your account, you think that money's all yours, but the reality is you should be withholding at least 25-30% of that income to cover your quarterly estimated tax payments and end-of-year tax bill.

Use Keeper's free quarterly tax calculator to estimate how much you should be setting aside.

We recommend opening an HYSA, setting aside 25-30% of your income for taxes in that income, and earning interest on the money sitting in that account. On $15,000 that's roughly $600 in interest earned in a year.

Keeper pro tip: Open a dedicated HYSA only for taxes. Separating it from your spending money and emergency fund is the single most effective way to avoid the April tax bill panic.

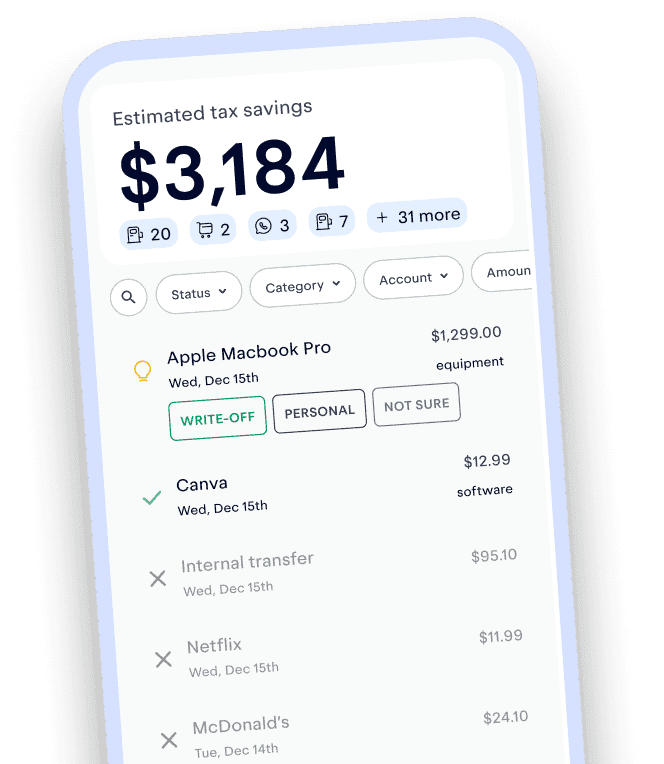

Track and claim every eligible deduction with Keeper

Keeper scans your accounts for write-offs and files your return — with tax pros reviewing every one.

Try it freeHow much should a self-employed person actually set aside for taxes?

The 25%–30% rule of thumb works for most people, but here's how to think about it, so you can apply it to your personal situation.

As a self-employed person, you owe the IRS two things:

Self-employment tax: 15.3% of net earnings (12.4% for Social Security on the first $184,500 of income in 2026, plus 2.9% for Medicare).

Federal income tax: your ordinary rate, which depends on your total taxable income and tax bracket.

Stack those, add state income tax if your state has one, and most freelancers land at an effective rate of 25%–35% of net business income. If you're in a no-income-tax state and a lower bracket, 25% is usually safe. If you're a higher earner in a state like California or New York, set aside closer to 35%.

Keeper's free tax rate calculator helps you estimate how much to set aside for your taxes.

When are quarterly taxes due in 2026?

The IRS expects estimated payments four times a year if you expect to owe $1,000 or more:

Quarter | Income period | Due date |

|---|---|---|

Q1 | Jan 1 – Mar 31, 2026 | April 15, 2026 |

Q2 | Apr 1 – May 31, 2026 | June 15, 2026 |

Q3 | Jun 1 – Aug 31, 2026 | September 15, 2026 |

Q4 | Sep 1 – Dec 31, 2026 | January 15, 2027 |

How to avoid an underpayment penalty (the safe harbor rule)

What's a top 5 horror movie moment for taxpayers? Underpaying the IRS. Well, there's something called the safe harbor rule for estimated tax payments that works in your favor.

See how much you could end up paying in penalties if you skip out on payments with our estimated tax penalty calculator.

You won't be penalized (even if you underpay) as long as you hit the IRS safe harbor:

Pay at least 90% of this year's tax, or

Pay 100% of last year's tax (110% if your prior-year AGI was over $150,000), whichever is smaller.

Wait... is high-yield savings interest taxable?

Well, yes. It is income earned after all.

The interest you earn in a high-yield savings account is taxable as ordinary income at your regular tax rate. Your bank will send you a Form 1099-INT if you earn $10 or more in interest during the year, and you report it on your Form 1040, even if you never withdrew the money.

Every year, someone discovers that HYSA interest is taxable and declares the whole thing a scam.

But taxes don't erase the income. They just take a slice of it.

If your savings account earns you $1,000 in interest, you don't hand all $1,000 over to the IRS. You pay tax on that income and keep the rest. Even after taxes, earning 4% is a lot better than earning 0%.

Think of it this way: nobody turns down a raise because they'll owe more taxes. HYSA interest works the same way.

How to put the whole thing on autopilot

The hardest part of the "save for taxes" habit isn't the math. It's remembering to do it on every single payment, and knowing what you actually owe.

That's where Keeper helps. Keeper securely links to your bank accounts to give you a real-time estimate of how much you expect to owe, automatically scans your expenses for tax deductions, and helps you estimate how much to pay in quarterly taxes, and lets you file directly when the deadline comes.

Over 1M Americans trust Keeper for their complex taxes

The #1 tax app for freelancers, gig workers, and self-employed filers.

Get started freeFAQs

What is the highest-paying high-yield savings account right now?

As of June 2026, Varo advertises the highest rate at up to 5.00% APY, though it applies only to the first $5,000 and requires qualifying direct deposits. For a high rate with no balance cap, Axos (up to 4.21%) and CIT Bank (4.10%) are among the leaders. Rates change often, so confirm before opening.

Are high-yield savings accounts safe?

Yes, as long as the account is FDIC-insured (banks) or NCUA-insured (credit unions). Your deposits are protected up to $250,000 per depositor, per institution.

Can I use a high-yield savings account to save for taxes?

Absolutely, and it's one of the smartest uses for one if you're self-employed. Move 25%–30% of each payment into a dedicated HYSA, pay your quarterly estimated taxes from it, and earn interest on the balance in the meantime.

Do I pay taxes on high-yield savings account interest?

Yes. HYSA interest is taxed as ordinary income, and your bank reports it on Form 1099-INT if you earn $10 or more in a year. You report it on your Form 1040 even if you didn't withdraw it.

How much should I set aside for self-employment taxes?

Most freelancers should set aside 25%–30% of net income to cover both self-employment tax (15.3%) and federal income tax. Higher earners or those in high-tax states should lean toward 35%.

Sign up for Tax University

Get the tax info they should have taught us in school.

Read next

Krislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces.

View full bio