Tax Deductible Expenses Every Rental Property Owner Should Know

If you own a rental property, chances are you're spending quite a bit to upkeep it. Most landlords know they can write off their mortgage interest and property taxes. What they often miss are the dozens of other deductible expenses hiding in plain sight: the miles driven to check on a property, the CPA fees to prepare your return, even the cost of marketing your rental. Here's our tax guide on expenses you should be deducting for your rental.

Krislyn ChanKrislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces.

Krislyn ChanKrislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces. Reviewed bya tax professionalThis content has been reviewed by an Enrolled Agent (EA) with the IRS — the highest credential awarded by the agency. Enrolled Agents are empowered to represent all taxpayers before the IRS, on all types of tax-related matters. Accountants who earn this certification have passed a comprehensive three-part exam on individual and business tax returns. To maintain EA status, they must stay up to date in the field by completing 72 hours of continuing education every three years.

Reviewed bya tax professionalThis content has been reviewed by an Enrolled Agent (EA) with the IRS — the highest credential awarded by the agency. Enrolled Agents are empowered to represent all taxpayers before the IRS, on all types of tax-related matters. Accountants who earn this certification have passed a comprehensive three-part exam on individual and business tax returns. To maintain EA status, they must stay up to date in the field by completing 72 hours of continuing education every three years.How rental income is taxed

Before diving into deductions, it's important to note that rental income is reported on Schedule E (Form 1040), and the IRS generally treats it as passive income, not earned income like a salary. This distinction matters a lot when it comes to losses, which we'll cover below.

Your taxable rental income = gross rent received minus deductible expenses. The goal isn't to avoid paying taxes altogether. It's to make sure you're only paying taxes on your actual economic profit, not on money you spent keeping the property running. After all, it takes money to make money, right?

12 tax deductible operating expenses

These are the day-to-day expenses you can write off in the tax year you pay them.

1. Mortgage interest

The interest portion of your mortgage payment is fully deductible, but the principal is not. This is one of the most significant deductions for most landlords, often running into the thousands annually. Note: You can only deduct interest, so look at your annual mortgage statement (Form 1098) to find the correct figure!

Keeper pro tip: For 2025, the business interest expense limitation under Section 163(j) may apply if your interest expense is substantial. The calculation now adds back depreciation, amortization, and depletion to adjusted taxable income when determining your limit. Most individual landlords with a single property won't hit this ceiling, but those with large portfolios should be aware.

2. Property taxes

State and local real estate taxes on your rental property are fully deductible as a rental expense. This is separate from (and in addition to) any property taxes you may deduct on your primary home via Schedule A!

3. Landlord insurance premiums

Landlord-specific insurance, sometimes called dwelling or hazard insurance, is deductible. This includes liability coverage, property insurance, flood or earthquake policies, and umbrella coverage tied to the rental activity. Standard homeowners insurance on a property you convert to a rental also qualifies once it's in service as a rental.

4. Repairs and maintenance

Routine repairs that keep the property in its existing condition are fully deductible. That includes things like fixing a leaky faucet, patching a section of roof, replacing a broken window pane, repainting interior walls, repairing an HVAC unit, or clearing a clogged drain.

However, there's an important distinction here to keep in mind: repairs are deductible immediately; improvements are not. An improvement adds value, extends the property's useful life, or adapts it to a new use. In that case, improvements must be depreciated over time. A simple example of this is replacing your windows.

Replacing a broken window pane is a repair;

Replacing all windows throughout the building is a capital improvement.

Make sure you don't trigger an audit on your Schedule E because of this distinction!

Keeper pro tip: The IRS provides a "de minimis safe harbor" that allows landlords to immediately expense items costing $2,500 or less per invoice, rather than capitalizing and depreciating them. This is especially useful for appliance replacements or small fixture upgrades.

5. Property management fees

If you hire a property management company, their fees, typically 8–10% of monthly rent, are fully deductible. This also includes tenant placement or leasing commissions paid to find new renters.

6. Advertising and tenant screening

Posting a listing on Airbnb, Zillow, or Apartments.com, running a local ad, or paying for a background and credit check on a prospective tenant are all deductible. Even the cost of a "For Rent" sign counts.

7. Utilities (that you pay!)

If you cover water, gas, electricity, trash removal, or sewer for your tenants, those amounts are deductible. One nuance: if a tenant pays a utility bill and deducts it from rent, that utility cost is still technically rental income to you, but you can then deduct it as a rental expense.

8. Professional and legal fees

Fees paid to a CPA or tax preparer specifically to prepare Part I of Schedule E are deductible as a rental expense in the year paid. Legal fees for evictions, lease drafting, or other landlord-tenant matters are also deductible. However, legal fees to defend or protect your title to the property, or to recover the property itself, cannot be deducted currently; they must be added to the property's cost basis.

9. HOA fees

If the property belongs to a homeowners association, the dues and assessments you pay are deductible as long as they cover ongoing operating costs (maintenance, common area upkeep). Special assessments that fund capital improvements to the property. like adding a new pool, are generally not immediately deductible.

10. Travel and mileage

Driving to your rental to show it to a prospective tenant, supervise repairs, collect rent, or conduct a move-in inspection qualifies as a deduction. For 2025, the IRS standard mileage rate is 70 cents per mile (up from 67 cents in 2024). You can also deduct actual expenses (gas, insurance, maintenance) over using the mileage method if you prefer. The best option is one that will net you the most tax savings. Lucky for you, we've written a helpful guide to break down when you should use the mileage vs expense method.

If you choose to track your mileage, you can use a simple spreadsheet (check out our free mileage log template) or track it with the Keeper app.

If you choose to use the actual expense method, Keeper connects to your accounts and credit cards to automatically flag and track your tax deductible expenses.

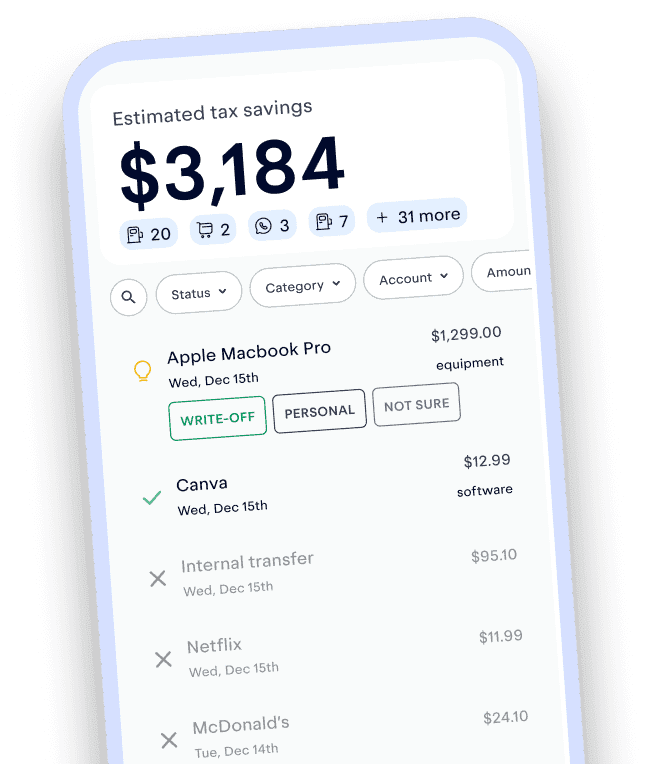

Track and claim every eligible deduction with Keeper

Keeper scans your accounts for write-offs and files your return — with tax pros reviewing every one.

Try it free11. Vacant property expenses

Here's one many landlords miss entirely: if your rental unit sits vacant while you're actively trying to rent it out, you can still deduct the operating expenses (including depreciation) during that period. You cannot deduct a hypothetical loss of rental income, but the actual costs of holding the property continue to be deductible.

12. Pre-rental expenses

If you incurred ordinary and necessary expenses to prepare a property for rental (landscaping, cleaning, minor repairs) before it was first placed in service, those costs are also deductible. The clock starts when the property is made available for rent, not when you actually receive your first tenant.

Depreciation is your largest deduction

The concept is straightforward: the IRS recognizes that rental buildings wear out over time, and allows you to deduct a portion of the building's cost each year, even if you're not writing a check for it. For residential rental property, depreciation is calculated using straight-line depreciation over 27.5 years. That means if your building's depreciable value (purchase price minus land value - land is never depreciable!) is $300,000, you can deduct roughly $10,909 per year.

When you purchase a rental property, you must allocate the purchase price between the land and the building. A property tax assessment or appraisal can help establish this split.

Keeper pro tip: Some landlords avoid claiming depreciation because they've heard it triggers a "recapture" tax when they sell. When you sell a rental property, the IRS "recaptures" previously claimed depreciation and taxes it at a maximum rate of 25%, which is higher than the typical long-term capital gains rate of 15–20%. The IRS requires depreciation recapture whether or not you actually claimed it. If you skip depreciation, you still owe the recapture tax at sale, and you gave up years of current deductions for nothing.

If you've missed depreciation in prior years, file IRS Form 3115 (Application for Change in Accounting Method) to catch up. A CPA can handle this retroactive correction. Need help? Book a call with a Keeper CPA.

OBBBA restored 100% bonus depreciation

One of the most significant tax changes for rental property owners in 2025 is the restoration of 100% bonus depreciation under the One Big Beautiful Bill (OBBBA), signed by President Trump in July 2025. For qualified property acquired and placed in service after January 19, 2025, investors can now deduct the full cost in Year 1, rather than spreading it over years.

Bonus depreciation applies to personal property components within a rental (appliances, carpeting, certain fixtures), not to the building structure itself (which still depreciates over 27.5 years). A cost segregation study, which is an engineering-based tax analysis, can help identify which components qualify for faster write-offs and is especially valuable for large property acquisitions.

Keeper pro tip: The study fee, typically $5,000–$15,000 for residential properties, is a deductible business expense in the year it's incurred!

The QBI deduction is a 20% write-off

Under Section 199A, qualifying landlords may be eligible to deduct up to 20% of net rental income as a Qualified Business Income (QBI) deduction. This is in addition to your regular expense deductions.

To qualify, your rental activity must rise to the level of a trade or business under IRS rules, or meet the safe harbor requirements established in Revenue Procedure 2019-38 (which requires, among other things, maintaining separate books and records and logging at least 250 hours per year in rental services). Not every landlord qualifies, and the rules are nuanced. But if you do qualify, a 20% deduction on net rental income is meaningful. This is a conversation worth having with your Keeper CPA!

Prevent an audit with good recordkeeping

The IRS can audit Schedule E returns, and without good records, you risk losing deductions you legitimately earned.

Make sure to track your personal vs rental expenses. You can use an app like Keeper to automatically track and categorize your tax deductible expenses.

Keep digital copies of your receipts. You can snap a pic and upload them into Keeper.

Retain records for at least seven years.

Software like Keeper can help you generate a clean paper trail for tax season by automatically tracking and categorizing your tax deductible expenses, keeping digital photos of your receipts and notes on your transactions, and adding those deductions directly to your tax return when you file.

Over 1M Americans trust Keeper for their complex taxes

The #1 tax app for freelancers, gig workers, and self-employed filers.

Get started freeRead next

The Short-Term Rental Tax Loophole Explained

What is the short-term rental tax loophole? Discover how high-earners can eliminate thousands in taxes, legally. Learn the IRS rules, real examples, and CPA strategies for 2025–2026.

Cost Segregation Studies for Rental Properties: What Every Investor Needs to Know

Do You Need To File a 1099 for Your Rental Property?

Krislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces.

View full bio