The QBI Tax Deduction: What Is It and Who Can Claim It?

The QBI deduction can mean a 20% tax break for self-employed people. Find out if you’re eligible and how to claim it in just two steps!

Justin W. Jones, EA, JDJustin is an IRS Enrolled Agent, allowing him to represent taxpayers before the IRS. He loves helping freelancers and small business owners save on taxes. He is also an attorney and works part-time with the Keeper Tax team.

Justin W. Jones, EA, JDJustin is an IRS Enrolled Agent, allowing him to represent taxpayers before the IRS. He loves helping freelancers and small business owners save on taxes. He is also an attorney and works part-time with the Keeper Tax team.

What is the qualified business income deduction?

The qualified business income (QBI) deduction is a tax break that lets business owners with pass-through income write off up to 20% of their taxable income. This ultimately lowers the amount of income tax they owe.

If not all of that made sense, don’t worry — we’ll get into what “pass-through income” means in a bit. For now, though, just know that your “qualified business income” is just the amount of taxable income your business earned.

Also known as Section 199A, the QBI deduction was added to the US Tax Code by the Tax Cuts and Jobs Act (TCJA). It’s been available to eligible freelancers, independent contractors, and business owners since January 1, 2018.

The history behind the QBI deduction

Workers with pass-through income have always had a unique tax advantage: Their business income is taxed at the owner’s individual tax rates instead of the much higher corporate tax rate of 35%. Since most taxpayers’ rates fall between 12 and 22%, this created a huge competitive edge.

However, that advantage went away after the TCJA lowered the corporate tax rate to 21%. People were understandably upset. Imagine carefully choosing your business’s entity structure based on the potential tax savings… all for Congress to take it away with one fell swoop.

The QBI deduction was the IRS’s solution. They figured a 20% deduction would be enough to quell people’s outrage.

How does the QBI deduction work?

There are two important things to note about the QBI deduction:

✓ It doesn’t matter if you take the standard deduction or itemize

Both options qualify you for the QBI deduction.

✓ It doesn’t lower your self-employment tax

The QBI deduction only lowers your income taxes, not your self-employment taxes.

To lower your self-employment taxes, take advantage of business write-offs! Anything you buy for work can be used to lower your taxable income.

Not sure what counts? You can use Keeper to scan your purchases and automatically deduct everything that’s an eligible business write-off in your industry.

Over 1M Americans trust Keeper for their complex taxes

The #1 tax app for freelancers, gig workers, and self-employed filers.

Get started free✓ It can impact retirement planning

You can’t apply the 20% QBI write-off to money that’s been put into a tax-deductible retirement plan, like a 401(k) or SEP-IRA.

Let’s take a step back to dig into the implications here. When self-employed people put money into their 401(k)s, the amount they contribute can be deducted from their business income. But because taking that deduction lowers their business income, it also lowers the amount of their QBI write-off. After all, 20% of $40,000 is less than 20% of $50,000.

Because of this, business owners are faced with a decision between short-term and long-term savings. If you forego your retirement savings in favor of more QBI, you’ll reduce the amount of tax you owe the IRS right now. But the trade off is, you’ll miss out on the long-term benefits of 401(k) contributions.

Who’s eligible for the QBI deduction?

Let’s zero in on the kinds of freelancers and business owners that are eligible for the deduction.

Business owners with pass-through income

A pass-through business is one that’s not subject to corporate income tax. Instead, all its income “passes through” to the owner, who reports it on their personal tax return.

People who have pass-through income include:

Sole proprietors: A single individual, often a freelancer or independent contractor, who owns an unincorporated business

Partnership members: Two or more people who made a formal agreement to run a business together, such as a law firm

S corporation shareholders: People who own interest in an S corp and report the company’s corporate income, losses, deductions, and credits on their personal tax returns

Limited Liability Company (LLC) members: Owners of an LLC that’s taxed as either a sole proprietorship, a partnership, or an S corp

Beneficial owners of a trust or estate: Not all trusts or estates qualify — more on that shortly

After seeing such a laundry list, you might be wondering, “What business owners don’t qualify?”

The answer: People with C corporations. Unlike pass-through businesses, C corps do pay corporate income taxes and therefore can’t claim the QBI deduction.

What tax write-offs can I claim?

People with qualified REIT dividends or PTP income

Business owners aren’t the only people who can benefit from the QBI deduction. Those with qualified dividends from a real estate investment trust (REIT) or income from a publicly traded partnership (PTP) can also claim a 20% QBI deduction.

If you have both types of income, these QBI benefits actually stack. For example, if you have a sole proprietorship for your freelance work and also receive qualified dividends from an REIT, you can deduct 20% from your freelance income and 20% from your REIT dividends.

Qualified REIT dividends must be held for more than 45 days. They don’t include capital gains or regular qualified dividends.

What doesn’t count as qualified business income?

For deduction purposes, these types of income are excluded from QBI:

Earnings from a W-2 job (if you’re work a side hustle)

Income from business outside of the United States

Interest income unrelated to a trade or business

Annuities received from something other than a trade or business

Guaranteed payments from a partnership

Investment items like capital gains, capital losses, or dividends

For a full list of what the IRS doesn’t consider qualified business income, head here.

Sign up for Tax University

Get the tax info they should have taught us in school.

How is the QBI deduction calculated?

Typically, your QBI deduction is the smaller amount between these two options:

20% of your QBI, plus 20% of your REIT dividends and PTP income

20% of your taxable income, minus net capital gains

If you’re a typical freelancer, independent contractor, or small business owner, that’s really all you need to know. Feel free to skip to the section on claiming your QBI deduction!

On the other hand, maybe you have a more complicated situation — like earning high self-employment income or working in certain industries like law or medicine. In that case, there will be limits placed on the amount of QBI you can claim.

There are also special circumstances with people who own multiple businesses.

Limitations on QBI deductions

If your taxable income is above a certain threshold — or generated by certain trades — you may only be able to claim a portion of the deduction. At certain levels, you stop being eligible for the deduction altogether.

Let’s go over when these limitations apply to the amount you can deduct.

If your taxable income is above the IRS’s thresholds

When it comes to the QBI deduction, there are actually two income thresholds you have to deal with.

The lower QBI threshold

The lower threshold is what you need to stay below to get the full 20% deduction. This income limit changes every year based on inflation.

In 2024, the limits are $191,950 for single filers and $383,900 for joint filers.

Once you hit these limits, your QBI deduction will start to “phase out,” meaning you only get a partial deduction. But you won’t yet hit a hard limit based on the amount you’re paying out in wages to your employees — which does apply once you reach the second income threshold.

The higher QBI threshold

At the second, higher income threshold, things start to change again. (Thanks, IRS!) In 2024, these income limits are:

$241,950 for single filers

$483,900 for joint filers

For most businesses, once you hit those numbers, your deduction will be capped at the greater of either:

50% of the W-2 wages paid by your business, or

25% of the W-2 wages, plus 2.5% of qualified depreciable property (like buildings and equipment)

There are exceptions based on your industry, though. (More on those below!)

Finding your QBI deduction after the higher threshold

To give an example, let’s say you have $300,000 of taxable income, $100,000 of which is from your business. You also paid $30,000 of wages and you own an office building — a qualified property — worth $480,000.

Normally, you would be able to claim a $20,000 QBI deduction on your business income of $100,000 ($100,000 x 0.20 = $20,000).

But because your taxable income exceeds the limit for single filers, you have to use the calculations above to figure out your QBI deduction. Here’s how that would look:

Option A: $30,000 x 0.50 = $15,000

Option B: ($30,000 x 0.25) + ($480,000 x 0.025) = $19,500

In this scenario, option B results in the higher deduction.

If you own a “specified service trade or business”

A specified service trade or business (SSTB) is any trade or business where the main asset is the skill or reputation of at least one employee or owner.

What counts as an SSTB?

SSTBs include service businesses in:

Healthcare

Law

Accounting

Athletics

Consulting

Performing arts

… and more. Check out the full list here.

How QBI limits work for SSTBs

The QBI deduction an SSTB can claim is also based on their income level and filing status. What makes the SSTB designation unfortunate, is that — unlike everybody else — you can’t claim any deduction after you hit the income ceiling.

Here are the figures for the 2024 tax year:

Filing status | Taxable income | Eligible QBI deduction |

|---|---|---|

Single tax filer | Less than $191,950 | 20% |

Single tax filer | $191,950 - $232,100 | Partial deduction |

Single tax filer | More than $232,100 | 0% |

Married filing jointly | Less than $383,900 | 20% |

Married filing jointly | $383,900 - $483,900 | Partial deduction |

Married filing jointly | More than $483,900 | 0% |

If you recently bought partnership interest

There’s also a limit to the QBI deduction that can be claimed by someone who recently acquired partnership interest. (It’s especially likely to apply to partners who own real estate businesses.)

Luckily, most small business owners don’t have to deal with this limit, because it’s a little complicated. It’s calculated as a percentage of their wages, plus a different percentage of the “unadjusted basis immediately after acquisition” (UBIA). “Unadjusted basis” just means how much it originally cost to purchase the partnership’s property.

In a nutshell, people in this situation have their QBI deduction capped at the sum of:

25% of the W-2 wages paid

2.5% of its UBIA

The UBIA used to calculate the partner’s QBI deduction must be calculated by the individual or entity that directly conducts the qualified business.

Now that we’re all clear on who can claim the QBI deduction — or portions of it — let’s move on to how you go about it.

For people with multiple businesses

If you own multiple pass-through businesses, you can opt to aggregate your business interests, which, in some circumstances, may give you a larger QBI deduction.

There are some limitations to who’s allowed to aggregate their businesses. For instance, your businesses can’t be SSTBs and need to be connected in some meaningful way. You can learn more here!

How to claim the QBI deduction

This is a dense subject, and there’s a lot to cover. It’s the rare case where you can’t see the trees for the forest, because the overall concept is so hard to grasp.

The solution? Let’s break down the steps of applying for the QBI deduction, which aren’t all that complicated.

Step #1: Determine your taxable income

Your taxable income is your total income minus any deductions you're entitled to claim, including your business write-offs and the standard deduction.

Even before your QBI deduction kicks in, you can lower your taxable income off the bat by keeping thorough expense records throughout the year. That way, you’ll know what you can write off.

If you haven’t been quite on top of your bookkeeping, don’t worry! The Keeper app offers a built-in deduction tracker that scans your purchases and finds qualifying business expenses for you. After everything's accounted for, you can file with Keeper too.

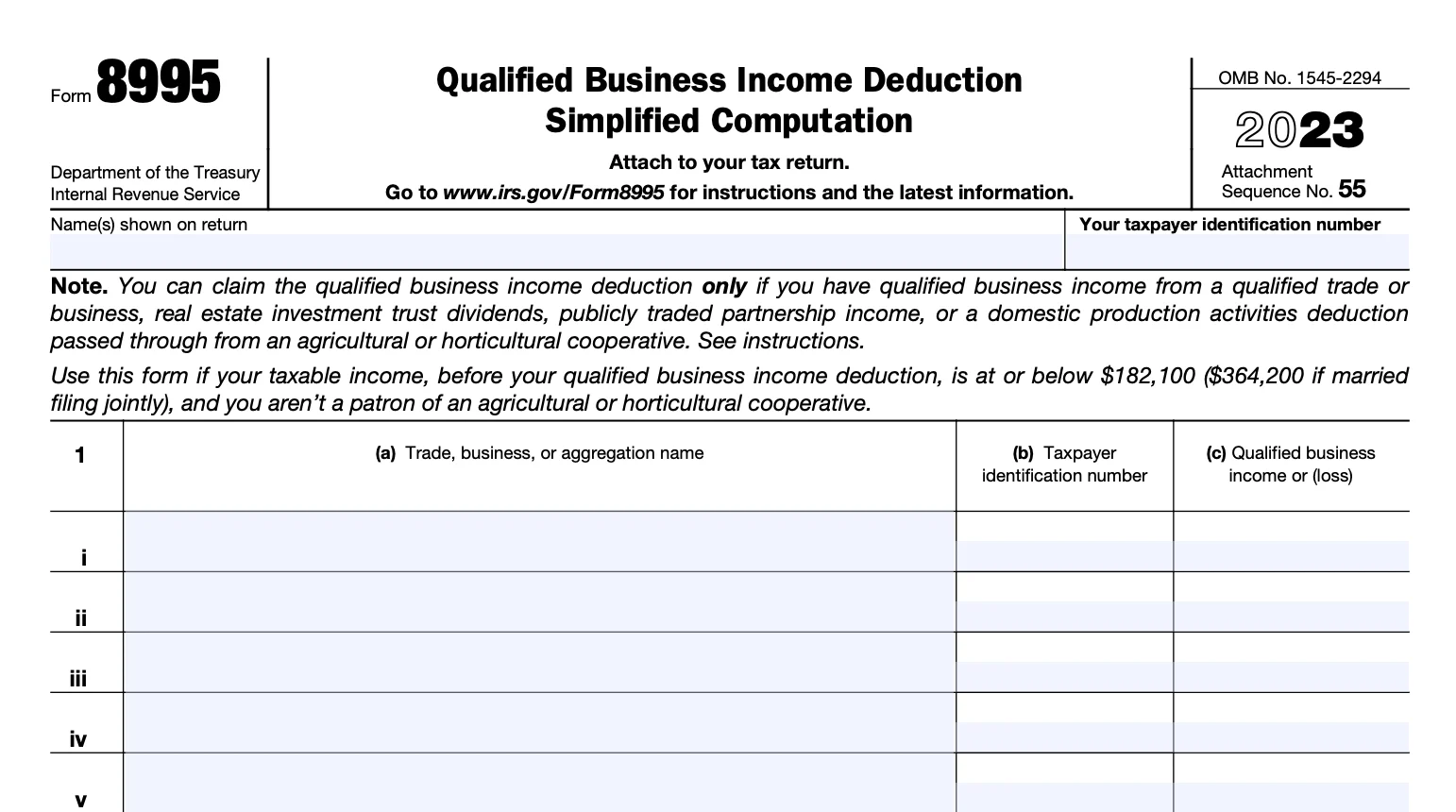

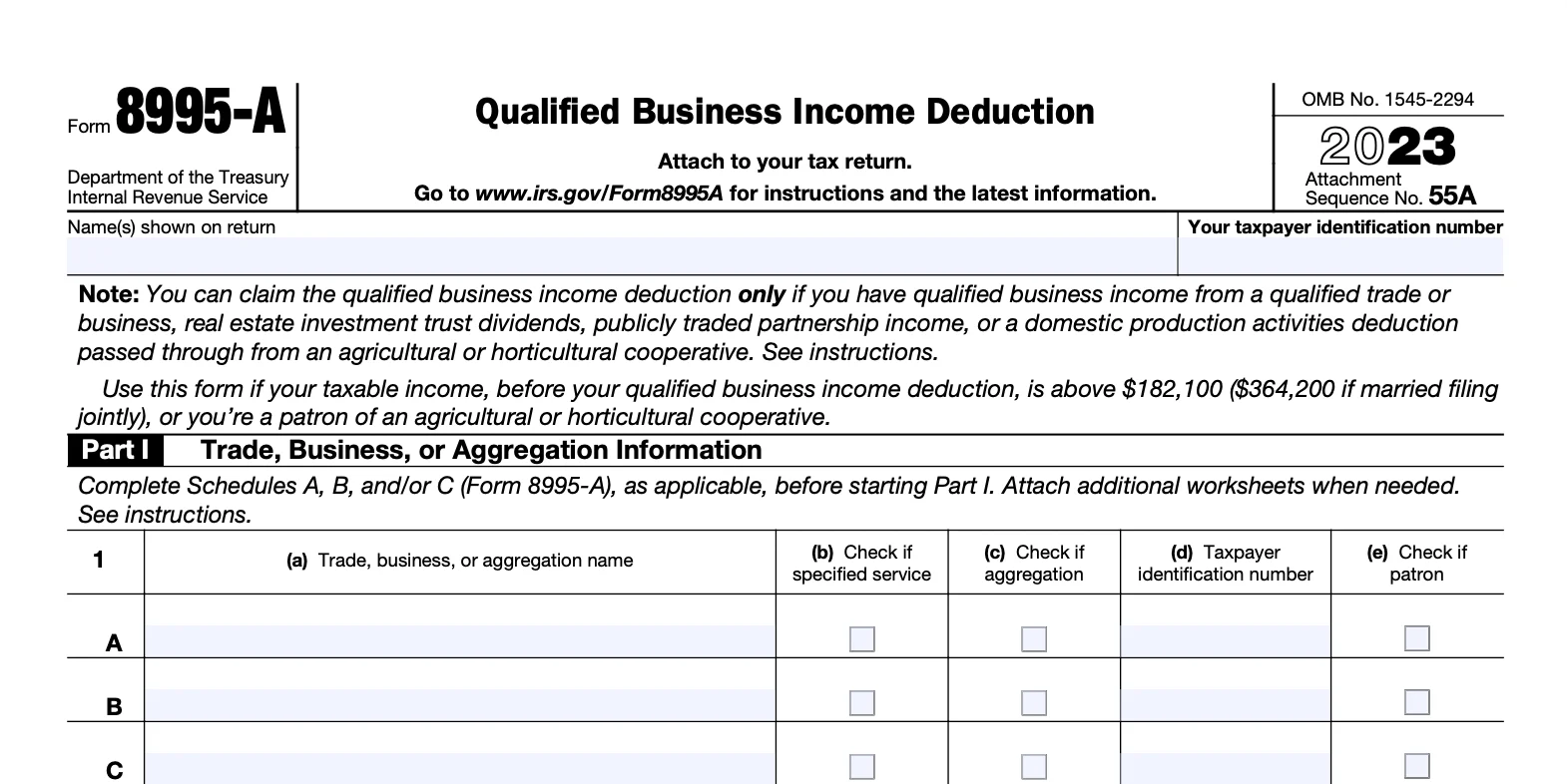

Step #2: Fill out Form 8995 or 8995-A

There are two forms you can use to apply for your QBI deduction: Form 8995 and Form 8995-A.

For 2024, use Form 8995 if you are:

A single filer with a taxable income at or below $191,150 before QBI deductions

A joint filer with a taxable income at or below $383,900 before QBI deductions

Use Form 8995-A if you are:

A single filer with a taxable income above $191,150 before QBI deductions

A joint filer with a taxable income above $383,900 before QBI deductions

And that’s it! Both of these forms have worksheets that will help you determine the amount of QBI deduction you’re eligible for. And once you’re done filling the relevant form out, make sure to attach it to your tax return when you send it off to the IRS.

Hopefully, you’re a little clear now about how the QBI deduction works — and feel ready to maximize it to your full advantage. If you still have questions, the IRS has a pretty thorough Q&A page dedicated to the deduction.

And if you’re looking for simpler explanations of complicated tax topics, our Keeper tax assistants are here for you! Download the app, and text your questions. You’ll get back an answer in plain English.

Read next

A Beginner's Guide to Self-Employment Taxes

Self-employment tax, also known as FICA, is the cost of Social Security and Medicare that is required of all self-employed individuals. Find out how to calculate, reduce, and pay this tax.

How To Deduct Write-Offs Without an LLC

Should You File Your Own Business Taxes?

Justin is an IRS Enrolled Agent, allowing him to represent taxpayers before the IRS. He loves helping freelancers and small business owners save on taxes. He is also an attorney and works part-time with the Keeper Tax team.

View full bio