What Freelancers Need to Know About Self-Employed Disability Insurance

If you’re self-employed, disability insurance can help cover your income if you have to stop working thanks to illness or injury. Learn how!

Margaret WackMargaret Wack is a freelance writer and poet. She’s covered topics including personal finance, insurance, small business and entrepreneurship, and loose leaf tea for US News & World Report, Investopedia, MoneyGeek, Money Under 30, Angi, Insurify, and ArtfulTea. When she’s not writing for work or pleasure, she’s usually curled up with a cup of tea and a good book.

Margaret WackMargaret Wack is a freelance writer and poet. She’s covered topics including personal finance, insurance, small business and entrepreneurship, and loose leaf tea for US News & World Report, Investopedia, MoneyGeek, Money Under 30, Angi, Insurify, and ArtfulTea. When she’s not writing for work or pleasure, she’s usually curled up with a cup of tea and a good book. Reviewed byIsaiah McCoy, CPAIsaiah McCoy is a Certified Public Accountant (CPA) in Miami, Florida with over a decade of experience in tax, accounting, and financial analysis. He holds a Bachelor of Science degree in accountancy and a Master of Taxation degree from Arizona State University. Isaiah has also earned a Master of Business Administration with a finance concentration from LSU Shreveport. Isaiah has worked within several industries, including public accounting (serving clients in the natural resources, real estate, and not-for-profit sectors), higher education, and healthcare. In his free time, he enjoys traveling and watching soccer and is fluent in Spanish.

Reviewed byIsaiah McCoy, CPAIsaiah McCoy is a Certified Public Accountant (CPA) in Miami, Florida with over a decade of experience in tax, accounting, and financial analysis. He holds a Bachelor of Science degree in accountancy and a Master of Taxation degree from Arizona State University. Isaiah has also earned a Master of Business Administration with a finance concentration from LSU Shreveport. Isaiah has worked within several industries, including public accounting (serving clients in the natural resources, real estate, and not-for-profit sectors), higher education, and healthcare. In his free time, he enjoys traveling and watching soccer and is fluent in Spanish.

How does disability insurance work?

If you were to suffer from a serious illness or injury that made you unable to work for months, could you and your family get by without your income? For many, the answer is no.

That’s where disability insurance coverage comes in. It supplements your lost income (and that of your business) until you can get back on your feet. You’ll generally pay a monthly premium to cover a percentage of your income — most commonly around 60%.

What does disability insurance cover?

If you’re not prone to illness or injury, you may not think you need disability insurance. But you might be surprised at what such a policy can cover. According to Jiten Puri, founder of PolicyAdvisor.com, “The most common claims for short-term disability are mental health issues, poisoning, and musculoskeletal injuries like strains or even carpal tunnel.”

So even if you’re just spending too many long hours hunched over your keyboard, a disability insurance policy could come in more handy than you think.

Do self-employed people need disability insurance?

Technically, no — although it can be incredibly helpful. Disability insurance isn’t required, and there are no fees or penalties for skipping this type of coverage.

To decide whether to purchase a policy, you should consider how much you depend on your freelance income — and how you would make ends meet if you were no longer able to work for a while.

Do side hustlers need self-employed disability insurance?

Like any insurance policy, disability insurance is all about protecting you from financial risk. Whether or not you should purchase a policy depends on how much financial risk you’d be running if you weren't able to work your side hustle.

For instance, if you have a side hustle baking pies that nets you a few hundred dollars a year, disability insurance may not be necessary. You’d manage without that income. The cost of disability insurance itself may even negate the financial benefits it would bring. (We’ll talk about how much you can expect to spend later!)

On the other hand, if your freelance income is more substantial, then a disability insurance policy may make more sense. For instance, if you run a landscaping company outside your day job that nets you an extra $30,000 per year, you may want to consider a policy.

Is disability insurance tax deductible for the self-employed?

Unfortunately, private disability insurance generally isn’t tax-deductible for freelancers. However, there are a few scenarios in which you might be able to deduct disability insurance premiums.

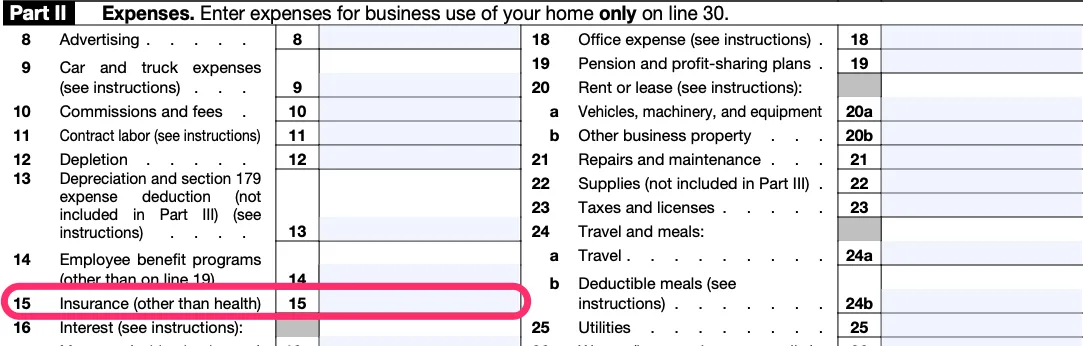

✓ If you pay for business overhead disability insurance

This type of insurance covers your business income, not your personal income, and premiums are tax-deductible. (More on this below.)

If you have this type of coverage, deduct it on line 15 of your Schedule C when you file taxes.

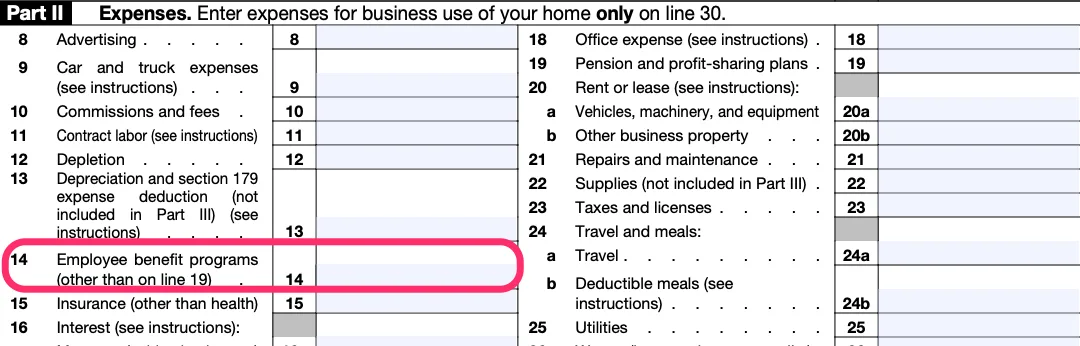

✓ If you offer personal disability insurance as a benefit to your employees

In this case, you can deduct disability insurance premiums as a business expense. You'll claim it on line 14 of your Schedule C.

Freelancers should also keep in mind that health insurance is deductible in the form of an income adjustment.

If you do end up purchasing disability insurance for employees, business overhead disability insurance, health insurance, or any of a number of other common business expenses, Keeper can help you keep track of it all.

The app will automatically scan your accounts for write-offs, including any applicable insurance premiums. At tax time, you can file right through the app.

Over 1M Americans trust Keeper for their complex taxes

The #1 tax app for freelancers, gig workers, and self-employed filers.

Get started freeTypes of disability insurance for the self-employed

There are a few different kinds of private disability insurance to keep in mind. First, there’s the difference between short-term and long-term coverage:

Short-term disability insurance protects you in the event of a temporary illness or injury

Long-term disability insurance protects you from a long-lasting or permanent illness or injury that impacts your ability to work in your chosen field

Both are types of personal disability insurance. That’s different from disability overhead insurance:

Personal disability insurance is designed to replace your own lost income

Disability overhead insurance covers expenses, like rent and payroll, so you can keep your business infrastructure in place until you’re ready to return to work.

Short-term disability insurance

Used by: Someone who can’t work for a few weeks

As the name implies, short-term disability coverage is designed to cover you for short-term illnesses and injuries. This type of insurance coverage generally lasts from a few weeks up to a few months.

Long-term disability insurance

Used by: Someone who can’t work for several months — or years

Long-term disability policies cover you if you can’t work for a longer time. This type of coverage typically doesn’t kick in until at least 90 days — when short-term disability insurance often leaves off.

Depending on your policy, long-term disability insurance coverage may last up until retirement age.

Disability overhead insurance

Used by: Someone who needs to cover business expenses while unable to work

If you have significant recurring business expenses in the way of payroll, rent, supplies, and other costs, you may want to consider disability overhead insurance.

This type of insurance covers the income you reinvest in your business — not the personal income you use to fund your living expenses. It can help your business to stay afloat financially for a time if you’re unable to work.

How disability overhead insurance is different from personal coverage

Personal disability insurance plans only cover your personal income and expenses. This type of coverage is usually enough for freelancers or independent contractors who don’t have much business overhead.

Benefits for personal disability insurance — both long-term and short-term — are based on your personal net income. That’s your take-home pay: the amount you actually pocket after taking out your business expenses.

In contrast, disability overhead covers what you spend on those business expenses.

For example, say a freelance consultant makes $60,000 a year, but spends $20,000 on office rent, supplies, business travel, and other expenses. In this scenario:

Their personal disability insurance covers the $40,000 they take home in profit

Their disability overhead insurance covers the $20,000 they spend to run their business

To cover the entirety of their gross income, they’d need both types of policies.

For an accurate sense of what you’re spending on your business, try Keeper. The app makes it easy to track your work-related expenses, so you can write them off at tax time and figure out if disability overhead insurance makes sense for you.

How much does disability insurance cost if you’re self-employed?

As a rule of thumb, expect to pay between 1% to 3% of your annual income for the coverage you need — generally in the form of a monthly premium. Exactly how much you pay for a private disability insurance policy depends on factors like:

How much you make

Your expenses, your health

Your age, among other factors

The percentage of your income the policy will cover

The amount that your disability insurance policy will cover is based on a combination of your current year's income and income from the last two years. If your freelance income fluctuates a lot, the amount that insurers will agree to cover tends to be more conservative.

In general, a policy will usually be cheaper with:

A smaller compensation plan

A shorter benefit term

A longer waiting period before you begin to receive benefits after filing a claim

On the other hand, plans will cost more with:

A larger benefits package

A longer benefit period

A shorter waiting period

Along with private insurance plans, you may qualify for government-sponsored disability benefits. Programs exist through the Social Security Administration for long-term disabilities and through certain states for pregnancies and short-term issues.

Social Security disability insurance (SSDI)

You may qualify for Social Security benefits even if you aren’t retired. If you’re disabled indefinitely and can’t work, then you can apply for monthly income payments from Social Security Disability Insurance (SSDI).

How much does SSDI cost?

Nothing! You won’t have to pay anything extra for since you’ve been paying into Social Security with your self-employment taxes (and payroll taxes if you're a side hustler) That’s why it’s worth checking to see if you qualify.

Track and claim every eligible deduction with Keeper

Keeper scans your accounts for write-offs and files your return — with tax pros reviewing every one.

Try it free“Freelancers who want their own disability insurance coverage should start by researching what kind of coverage they may qualify for under Social Security. From there, they can look to supplement that with their own individual policy,” recommended Puri, the PolicyAdvisor.com founder.

How to qualify for SSDI

Self-employed workers will only qualify if they meet certain requirements. You need to:

Have worked jobs covered by Social Security

Have a medical condition that meets Social Security’s definition of disability

Because the requirements are so stringent, SSDI is often more difficult to obtain benefits from than a private disability insurance policy. That’s why it’s worth considering other options for disability insurance coverage, including private disability insurance and state-run programs for short-term family and medical leave.

State-sponsored disability insurance and paid family and medical leave

Depending on where you live, you may be able to pay into your state’s temporary disability insurance program. These programs are designed to provide coverage for:

Short-term illnesses

Parental leave

Other temporary issues

Sign up for Tax University

Get the tax info they should have taught us in school.

What states offer disability insurance?

States that offer short-term coverage programs include:

Maine (starting in 2026)

How much does state-sponsored coverage cost?

If you live in a state that offers this type of program, it’s often a very good deal. Freelancers typically pay only a small percentage of their yearly earnings in exchange for temporary disability insurance.

Exact costs and coverage amounts vary depending on the state, but freelancers can generally buy in by paying a small premium for a certain period of time. For instance, in Washington, freelancers must agree to pay 0.58% of their income for three years. In exchange, they can receive up to 90% of their weekly income for up to 12 weeks after a qualifying event.

Similarly, California’s Disability Insurance Elective Coverage allows small business owners and independent contractors to pay a premium in order to obtain disability insurance. Paid family leave coverage for up to 39 weeks.

How to choose the right disability insurance plan

The right disability insurance plan depends on your own unique financial circumstances.

For example, if you have an emergency fund, then you can afford to wait longer until you receive your first benefit income check. If your emergency fund is big enough to cover three months of expenses, you may want to opt for a longer waiting period so you can pay less on your monthly premium.

Disability insurance isn't a must-have for every freelancer or side hustlerBut if you can’t make do without your self-employment income, then paying for a policy can keep you afloat in an emergency. Without one, even a simple case of carpal tunnel could potentially put your family in financial jeopardy.

Between personal plans, business overhead insurance, and state-sponsored programs, you have plenty of ways to secure a financial safety net.

Read next

Liability Insurance for Independent Contractors: What You Need to Know

Liability insurance can protect you from financial risk if you have a side hustle or business. Here's how it works, how much it costs, and the best places to shop.

How To Claim Your Self-Employed Health Insurance Deduction

The Last Schedule C Guide You'll Ever Need

Margaret Wack is a freelance writer and poet. She’s covered topics including personal finance, insurance, small business and entrepreneurship, and loose leaf tea for US News & World Report, Investopedia, MoneyGeek, Money Under 30, Angi, Insurify, and ArtfulTea. When she’s not writing for work or pleasure, she’s usually curled up with a cup of tea and a good book.

View full bio