The 16 Best Banks for a Small Business (And How To Pick One)

Freelancing or starting a company? It’s vital to choose the right bank for your small business. Learn what to look for — and to avoid.

Christian DavisChristian is a copywriter from Portland, Oregon that specializes in financial writing. He has published books, and loves to help independent contractors save money on their taxes.

Christian DavisChristian is a copywriter from Portland, Oregon that specializes in financial writing. He has published books, and loves to help independent contractors save money on their taxes.

Do you need a separate small business bank account?

That depends on the size of your business.

If you’re launching a formal company, with employees and an office or storefront: Yes, absolutely.

However, for independent contractors, freelancers, and other 1099 workers, a business checking account is usually more headache than it’s worth. You can honestly keep doing things through your personal account.

But what about tracking business expenses?

Many people will tell all self-employed people that they need a separate business account. They cite tracking business expenses as the main benefit.

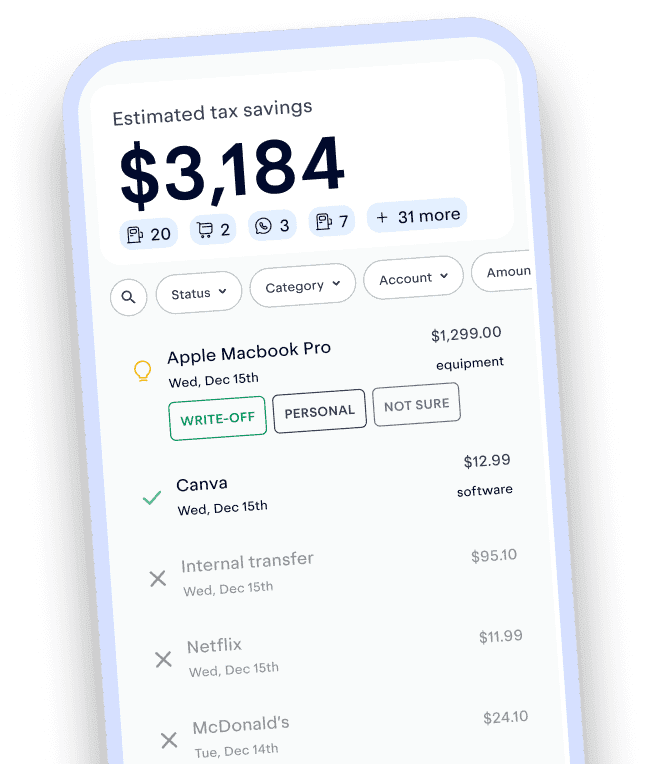

This isn’t a bad idea. But there are easier ways for independent contractors to keep an eye on business purchases! Like Keeper, which scans your transactions, marking the ones for your business and ignoring the rest. You can even file your taxes right in the app.

Track and claim every eligible deduction with Keeper

Keeper scans your accounts for write-offs and files your return — with tax pros reviewing every one.

Try it freeThis lets freelancers (especially people with side hustles) stay agile. They won't have to fuss with separating their personal and business finances.

Which bank is best for opening a small business account?

If you do need a separate business account, though, it’s important to know your options.

We combed through the terms of 16 top banks, assessing their usefulness to small businesses.

There is no one “best” bank for all businesses. It will always depend on your business's specific needs

For example, an already-established business might not need to worry as much about getting a business loan as one just starting out. On the other hand, it will need to keep a careful eye on how many free transactions it gets per month!

Check out the summaries below to learn more about each financial institution, including what additional features they offer for small businesses.

1. Capital One

Best if: You plan to make a lot of business purchases

Maintenance fees: $3-15/month

APY: 0.2% (first year only)

Transactions per cycle: Unlimited

Deposits per cycle: $5,000

Interest-earning checking account? ✘ No

Capital One is famous for its 2% cash back Spark Visa credit card.

Between that and its unlimited free transactions per monthly cycle, Capital One is a solid choice for high-activity businesses looking to earn back some of their expenses.

2. Wells Fargo

Best if: If you do business all across the country

Maintenance Fees: $5-$75/month

APY: 0.01%

Transactions per cycle: 100-250

Deposits per cycle: $5,000

Interest-earning checking account? ✓ Yes

One of the most popular banks for small business loans, Wells Fargo offers many different account types and lines of credit for businesses to choose from.

That, plus its extensive networks of branches and ATMs, makes it a top-notch choice for businesses of all sizes.

3. Novo

Best if: You’re always on the go and need powerful online capabilities

Maintenance fees: $0

APY: N/A

Transactions per cycle: Unlimited

Deposits per cycle: Unlimited Incoming Bank Deposits, Check Deposits up to $40,000

Interest-earning checking account? ✘ No

With no sneaky fees or minimum balance, Novo is ideal for small business owners who value simplicity and want to keep everything in one place. Novo’s free digital checking account comes with a debit card, automated budgeting, unlimited invoicing, and direct integrations with popular business tools you already use, like Stripe, Quickbooks, or Xero.

4. Chase

Best if: You’re a retailer looking to scale up

Maintenance fees: $15-$30/month

APY: 0.01% -0.02%

Transactions per cycle: Data Not Available

Deposits per cycle: Data Not Available

Interest-earning checking account? ✘ No

Best known for their high-reward credit cards, Chase Bank offers a variety of banking solutions, such as small business lending, and merchant services.

Add in numerous branches and ATMs nationwide, and Chase becomes a go-to bank for businesses.

4. Citibank

Best if: You need a big bank with solid mobile support

Maintenance fees: $15-$22/month

APY: Data Not Available

Transactions per cycle: 200-500

Deposits per cycle: $10,000-$20,000

Interest-earning checking account? ✓ Yes

Citibank is another long-running traditional bank with many international locations. Citibank was named the best bank for mobile cash management by Global Finance Magazine, so it's a good option if you want access to cutting-edge digital tools.

They’re also recognized as the best bank for payments and collections.

5. NorthOne

Best if: You want to integrate with other business tools

Maintenance fees: $0-$20/month

APY: None

Transactions per cycle: Unlimited fee-free transactions

Deposits per cycle: Unlimited ACH deposits, $5,000 in cash deposits, $50,000 in mobile check deposits

Interest-earning checking account? No

NorthOne is an all-in-one banking solution that lets you handle sales, payments, and business budgeting in one place. If you want to stay organized while still enjoying the benefits of automation, this is a great pick for you.

6. Baselane

Best if: You make a living through real estate investment

Maintenance fees: $0/month

APY: 4.25%

Transactions per cycle: Unlimited

Deposits per cycle: $25,000/day and $100,000/month for ACH deposits; no limit on other deposits

Interest-earning checking account? ✓ Yes

Built specifically for landlords and real estate investors, Baselane makes it easy to collect your rent. With this tech-forward option, you can use auto-categorization to divvy up your income by property — or sort them into various virtual accounts yourself. (Think of these as envelopes that help you stay organized.) You also get free wire transfers and ACH payments.

Meanwhile, 5% cash back from Home Depot makes it easy to keep your tenants happy and your properties ship-shape.

7. Lili

Best if: You want to understand how all the pieces of your business fit together

Maintenance fees: $0/month (Basic plan), $9/month (Pro plan), $20/month (Smart plan), $35 (Premium plan)

APY: 3.65%

Transactions per cycle: Unlimited inbound; $20,000/day and $100,000/month outbound

Deposits per cycle: $10.000/day and $50,000/month (mobile); $1,000/day and $9,000/month (cash)

Interest-earning checking account? ✓ Yes

If you want a Visa Business Debit card and no-fee access to ATMs, Lili’s free Basic plan is a solid pick. Its Pro plan, though, offers more than just banking. It lets you handle all the financial nuts and bolts of your business on a single screen — from invoicing clients to setting money aside for taxes. With the Smart plan, you'll also have access to smart bookkeeping features, like income and expense sorting.

One perk worth noting: If you overdraft your debit card by up to $200, Lili will cover it.

8. Axos Bank

Best if: You’re looking to grow your account through interest alone

Maintenance fees: $0-$10/month

APY: 0.81%

Transactions per cycle: 100-Unlimited

Deposits per cycle: Data Not Available

Interest-earning checking account? ✘ No

It’s famous for its 0.8% APY on their Business Interest Checking account. The low fees are a high-quality bonus too. Keep in mind: It's a fully online business, with zero brick and mortar locations for you to visit in person.

Unless you want local branches, Axos Bank is a solid choice for high yield account lovers.

9. First Citizens Bank

Best if: You’re a Southern business looking for loans

Maintenance fees: $0-$25/month

APY: Data Not Available

Transactions per cycle: 150-500

Deposits per cycle: $5,000

Interest-earning checking account? ✘ No

While First Citizens isn’t available everywhere, it ranks as one of the top two large banks featured here in terms of how much money it funnels into small businesses. Almost 28% of this bank’s portfolio centers on small business loans.

10. Bank of the West

Best if: You need business loans on the West coast

Maintenance fees: $10-$25/month

APY: Data Not Available

Transactions per cycle: 50-150

Deposits per cycle: $2,500-$5,000

Interest-earning checking account? ✘ No

The other big bank devoting a large percentage of its money toward small business loans. Bank of the West has over $5 billion out in small business loans.

11. Digital Federal Credit Union

Best if: You want the low costs of a credit union

Maintenance fees: None

APY: Up to 0.10%

Transactions per cycle: Data Not Available

Deposits per cycle: 20/day

Interest-earning checking account? ✓ Yes

While not technically a bank, a credit union like this one is a solid choice as a business banking solution. Credit unions usually offer higher interest rates and little to no fees. Their small business bank accounts can vary greatly, though.

Digital Federal Credit Union is a solid small business choice. If you're scoping out other credit unions, though, it's a good idea to do your research.

12. BlueVine

Best if: You’re a tech-savvy freelancer looking to earn big interest

Maintenance fees: None

APY: 1.2%

Transactions per cycle: Unlimited

Deposits per cycle: Data Not Available

Interest-earning checking account? ✓ Yes

Boasting the highest APY rate of our list by far, BlueVine is a good solution for young entrepreneurs looking for an online bank — without the typical BS of countless fees and impenetrable customer support.

13. First Home Bank

Best if: You need a fast business loan

Maintenance fees: None

APY: Data Not Available

Transactions per cycle: 250

Deposits per cycle: $7,500

Interest-earning checking account? ✓ Yes

First Home Bank offers multiple types of Small Business Administration (SBA) loans.

In fact, First Home is recognized as a Preferred Lender by the SBA. That makes the loan approval process quicker than usual.

14. KeyBank

Best if: Your business makes a lot of deposits a month

Maintenance fees: $5-$25/month

APY: 0.01%

Transactions per cycle: 100-500

Deposits per cycle: $25,000

Interest-earning checking account? ✓ Yes

If your small business is already established, KeyBank may well be the choice for you. This bank lets you deposit up to $25,000 per monthly cycle — more than any other bank on our list.

However, it doesn’t offer as many business loans as other banks.

15. US Bank

Best if: You need to expand quickly, especially with startup equipment

Maintenance fees: $0-$30/month

APY: 0.01%

Transactions per cycle: 150-500

Deposits per cycle: 25-200 deposits

Interest-earning checking account? ✓ Yes

US Bank’s Quick Loans offer a mighty incentive to startups and new businesses.

While most loans require business history (sometimes years’ worth), Quick Loans focus on loans for equipment, vehicles, and expansion. These let you get your business off the ground faster.

16. Square

Best if: You do a lot of point-of-sale business

Maintenance fees: None

APY: 0.50%

Transactions per cycle: Data not available

Deposits per cycle: Data not available

Interest-earning checking account? ✘ No

Good for merchants and independent artists with lots of vendor or convention sales.

What makes Square so appealing is its easy integration with its POS system and payroll. Essentially, it’s more than just a bank: Square provides a full financial setup for small sellers.

What should a small business look for in a bank?

Self-employed people and small business owners have unique banking needs. However, you might have different needs, depending on your industry, how big your business is, where you’re located, and how tech-savvy you are.

These are the main things you’ll want to consider when opening a business bank account:

Minimum balance requirements

The number of free transactions and deposits you get per statement cycle

A high Annual Percentage Yield (APY)

Low monthly maintenance fees

The quality of their mobile app and online banking services, for features like mobile check deposit

Access to customer service

Low interest rates

High cash back rates on business credit card

Ease of opening a business bank account

Whether you want brick and mortar bank or prefer an online platform

Low foreign transaction fees for business outside the US

Don’t be afraid to ask questions about your specific business needs. After all, no one knows your business like you do!

Any bank worth its salt will be happy to address your concerns. If they’re not, it’s better to know before you open that account.

The one universal consideration is that all bank accounts should also be FDIC insured — especially business accounts. If you’re looking to open an account and it’s not, run away and don’t look back.

Are small banks better for small businesses?

On average, yes.

Small banks are much more likely to approve small business loans than their larger counterparts. They know the needs of the community, and they’ll assess loan requests based on a human analysis rather than a cold algorithm.

Of course, size isn't the most important factor. There will always be bad small banks and good big banks — so don’t open an account with a bank just because they’re small. Always review the terms, conditions, and fees before signing any papers.

When to go with a big bank

Don’t ignore big banks completely! The good news is, they also sometimes give you extra peaks, like introductory offers for new customers. And depending on the needs of your business, having a known name and easy access to branches and ATMs across the country can be an advantage.

As you can see, there’s a lot of factors to consider when weighing the pros and cons of a bank for your small business. But so long as you keep your unique business needs in mind, the options that aren’t right for you should fall away pretty quickly.

And remember, you don’t need to stick with the first bank you choose if you don’t like it. Banks should want your business — if they don’t, it’s their loss when you switch to a competitor!

Sign up for Tax University

Get the tax info they should have taught us in school.

Read next

How To Open a Small Business Bank Account: Everything You Need to Know

Ready to open a business bank account? Here’s what you should know before applying (and a checklist for figuring out if you need one)!

Are Bank Fees Tax-Deductible? How To Save on Overdraft Fees and More

5 Best Receipt Apps for Small Businesses and Freelancers

Christian is a copywriter from Portland, Oregon that specializes in financial writing. He has published books, and loves to help independent contractors save money on their taxes.

View full bio