Solo 401(k) vs. SEP IRA: What's the Best Plan for Your Freelance Income?

A solo 401(k) will save most freelancers more money on their taxes, but a SEP IRA could be the better option for you. Find out which is the right choice.

Neeraja Viswanathan, JDNeeraja Viswanathan is an attorney and freelance writer who specializes in writing about apps that help small businesses with their marketing, accounting, and tax issues. In her free time, she rides horses, reads too many novels, and writes about film adaptations on www.mysteryonscreen.com

Neeraja Viswanathan, JDNeeraja Viswanathan is an attorney and freelance writer who specializes in writing about apps that help small businesses with their marketing, accounting, and tax issues. In her free time, she rides horses, reads too many novels, and writes about film adaptations on www.mysteryonscreen.com Reviewed byIsaiah McCoy, CPAIsaiah McCoy is a Certified Public Accountant (CPA) in Miami, Florida with over a decade of experience in tax, accounting, and financial analysis. He holds a Bachelor of Science degree in accountancy and a Master of Taxation degree from Arizona State University. Isaiah has also earned a Master of Business Administration with a finance concentration from LSU Shreveport. Isaiah has worked within several industries, including public accounting (serving clients in the natural resources, real estate, and not-for-profit sectors), higher education, and healthcare. In his free time, he enjoys traveling and watching soccer and is fluent in Spanish.

Reviewed byIsaiah McCoy, CPAIsaiah McCoy is a Certified Public Accountant (CPA) in Miami, Florida with over a decade of experience in tax, accounting, and financial analysis. He holds a Bachelor of Science degree in accountancy and a Master of Taxation degree from Arizona State University. Isaiah has also earned a Master of Business Administration with a finance concentration from LSU Shreveport. Isaiah has worked within several industries, including public accounting (serving clients in the natural resources, real estate, and not-for-profit sectors), higher education, and healthcare. In his free time, he enjoys traveling and watching soccer and is fluent in Spanish.

Why do you need a retirement plan as a freelancer?

These plans provide big cushions after you retire, and they come with tax breaks that can save you a considerable amount of money when you do your taxes. You can even start contributing to them before your business is profitable.

Even better, the two best retirement plan options for freelancers allow far more generous contributions than traditional IRAs or employee-sponsored retirement plans: $70,000 for 2025, instead of $7,000 for an IRA or $23,500 for a 401(k).

These are the solo 401(k) and the SEP IRA.

What is the solo 401(k)?

The solo 401(k) (also called a one-participant 401(k) or individual 401(k)) works exactly like a corporate 401(k), except you play both roles: you're the employee making salary deferrals and the employer making profit-sharing contributions. That dual-role structure is what makes it so powerful.

Who can start a solo 401(k)?

Anyone who makes some money from self-employment (literally any amount counts) can set up a solo 401(k), as long as they don’t have any full-time employees. You don’t need to have an LLC or a business license.

How much can you contribute per year?

As of 2025, the maximum amount you can contribute to a Solo 401(k) is $70,000. That includes both the amount you’re contributing as an employee, and the amount you’re contributing as your own employer.

As an employee

Your employee contribution, called an “employee salary deferral,” can total $23,500 in 2025, and this can be up to 100% of the net profits from your side hustle or business. That means that, if you earn less than $23,500, you’re free to put it all into a solo 401(k) and avoid paying taxes on it for the year.

If you’re 50 years old or older in 2025, you can also add an extra $7,500 a year, in what’s called in “catch-up contributions,” each year.

Keeper pro tip: The "super catch-up" window is very narrow. Only the four calendar years in which you are ages 60, 61, 62, and 63. Once you turn 64, you revert to the standard catch-up amount. If you're in that window, this is one of the highest-leverage tax planning opportunities available to you.

As an employer

Up to 25% of net self-employment income (or roughly 20% for sole proprietors after SE tax adjustments).

Solo 401(k) — Employee (Salary Deferral) Contributions

Tax Year | Under 50 | Age 50–59 or 64+ | Age 60–63 ("Super Catch-Up") |

|---|---|---|---|

2025 | $23,500 | $31,000 | $34,750 |

2026 | $24,500 | $32,500 | $35,750 |

Solo 401(k) — Total Combined Maximum (Employee + Employer)

Tax Year | Under 50 | Age 50–59 or 64+ | Age 60–63 ("Super Catch-Up") |

|---|---|---|---|

2025 | $70,000 | $77,500 | $81,250 |

2026 | $72,000 | $80,000 | $83,250 |

SEP IRA — Annual Contribution Limits

Tax Year | Maximum Contribution | Catch-Up Contributions |

|---|---|---|

2025 | 25% of compensation, up to $70,000 | None |

2026 | 25% of compensation, up to $72,000 | None |

Solo 401(k) vs. SEP IRA — Side-by-Side Comparison

Feature | Solo 401(k) | SEP IRA |

|---|---|---|

2025 Max (under 50) | $70,000 | $70,000 |

2026 Max (under 50) | $72,000 | $72,000 |

Catch-Up (50–59, 64+) | +$7,500 (2025) / +$8,000 (2026) | None |

Super Catch-Up (60–63) | +$11,250 | None |

Roth Option | Yes (well-established) | Yes (since 2023, less widely available) |

Roth Catch-Up Mandate (2026+) | Yes, if W-2 wages >$145K prior year | N/A |

RMD Start Age | 73 | 73 |

Loans Permitted | Yes (if plan allows) | No |

Employees Allowed | No (except spouse) | Yes |

Setup Deadline | Tax return due date (+ extensions) for employer/profit-sharing contributions | Tax return due date (+ extensions) |

Annual IRS Filing | Form 5500-EZ if assets >$250K | None in most cases |

What is the SEP IRA?

A SEP IRA is a profit-sharing retirement plan for self-employed individuals. (SEP stands for “Simplified Employee Pension.”)

It's basically a traditional employee pension plan, which means it’s ideal for small businesses with employees. It’s also a great option for someone who has already reached the contribution limit on their day job’s 401(k).

You contribute as the employer, not as an employee. It's fast to set up, cheap to maintain, and very flexible. You can contribute anywhere from 0% to 25% of income each year.

Who can start a SEP IRA?

To qualify for a SEP IRA, you have to:

Be at least 21 years old

Have earned at least $600 from self-employed work in the last year

Have done the same self-employed work for three of the past five years

How much can you contribute per year?

As of 2025, you can contribute 25% of your salary, up to $70,000. That’s a lot more than what you can contribute to traditional or Roth IRAs. That limit is $7,500 in 2025. In 2026, you can contribute up to $72,000.

Keeper pro tip: Because the SEP IRA employer contribution is calculated as a percentage of net income, and because you won't know your final net income until the year is over, it's generally impossible to front-load your contributions. You contribute in one lump sum, often when filing your tax return. The solo 401(k) employee deferral, by contrast, can be contributed at any time.

What tax breaks can you get with a solo 401(k) or SEP IRA?

Both types of accounts can help you reduce your tax bill, because the money you put in can be shielded from taxation. For example, if you earn $50,000 from freelancing and put $15,000 in a retirement account, your taxable income will only be $35,000.

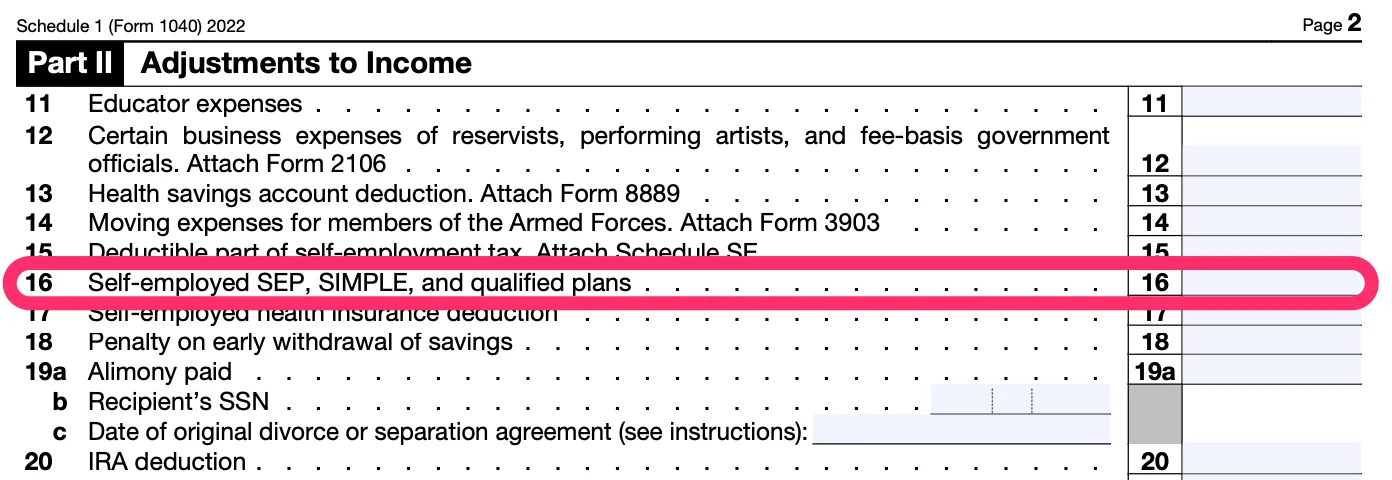

To claim this tax deduction, you’ll report your contributions on line 16 of Schedule 1 of your Form 1040 tax return.

If you’re a freelancer or side hustler, file through Keeper, and we’ll make sure your retirement savings are helping you save at tax time. And while we’re at it, our software — designed specifically for self-employed people — will translate your business expenses into tax savings too.

Track and claim every eligible deduction with Keeper

Keeper scans your accounts for write-offs and files your return — with tax pros reviewing every one.

Try it freeThe more you put into your retirement account, the more you’ll save on taxes. For most people, solo 401(k)s offer better tax benefits than SEP IRAs, thanks to more flexibility in how you can contribute, plus a Roth option.

In addition, your contributions might also qualify for the Retirement Savings Contribution Credit, or Saver’s Credit, if your adjusted gross income is less than $40,250 (filing single), or $80,500 (married filing jointly).

Tax benefits of a solo 401(k)

The Solo 401(k) generally offers more generous tax breaks because it can be funded from two different sources. As mentioned, these are:

Up to 25% from your contribution as an employer

Up to $23,500 (2025) / $24,500 (2026) from your contribution as an employee (with an additional $7,500 (2025) / $8,000 (2026) in catch-up contributions if you’re over 50)

An additional $11,250 if you're between 60-63

The overall IRS limit for contribution is $70,000 (under 50), $77,500 (age 50-59 or 64+), $81,250 (61-64).

Plus, a solo 401(k) lets you make post-tax Roth contributions on the employee side — which means you won’t have to pay taxes on that money when you withdraw it.

Tax benefits of a SEP IRA

Unlike with a solo 401(k), you can only contribute to this account from the employer side. The SEP IRA contribution limit is 25% of your income, or $70,000 for 2025 ($72,000 for 2026). This limits how much you can contribute, unless your income is high enough.

For self-employed sole proprietors, the effective rate works out to roughly 20% of net earnings after accounting for the self-employment tax deduction — so you'd need about $350,000 in net income to max it out.

Which retirement account has the best tax advantages?

In general, a solo 401(k) offers bigger tax breaks, since you can fund the account from two sources.

For example, say that your side hustle brings in $50,000 a year. Your day job pays the bills, so you want to save as much of your freelance income as possible. Here’s how the two accounts compare:

Solo 401(k): You can contribute $23,500 as an employee, plus 25% of your income, or $12,500.

SEP IRA: You can only contribute the $12,500 from the employer side.

Note that the employee-side contribution of $23,500 applies to all your 401(k) plans. So if you also have a 401(k) through your day job, your contribution to that account plus your solo 401(k) is capped at a combined $23,500.

Over 1M Americans trust Keeper for their complex taxes

The #1 tax app for freelancers, gig workers, and self-employed filers.

Get started freeIs a solo 401(k) or SEP IRA better for you?

Most freelancers will save more on their taxes with a 401(k). But ultimately, the best choice for any freelancer depends “on how much they are able to contribute, and how much time they have to dedicate to the management of the plan,“ said Houston-based CPA Thomas PM Perry.

In other words, let your personal priorities guide you. To help you figure those out, here are 10 possible scenarios where one plan is definitely a better choice than the other. See which ones describe your current situation best — that’s probably the better option for you:

You want to maximize contributions on a moderate income → Solo 401(k)

This is the core advantage of the solo 401(k). Because you contribute as both employer and employee, you can shelter far more income at lower earnings levels than a SEP IRA allows.

Example: Freelancer earns $50,000 net.

Solo 401(k): $23,500 employee deferral + ~$9,293 employer contribution = ~$32,793

SEP IRA: 20% × $50,000 net (after SE tax adjustment) = ~$9,293

The difference is substantial. The solo 401(k) wins decisively here.

You have (or plan to hire) full-time employees → SEP IRA

A solo 401(k) cannot cover employees who work more than 1,000 hours per year. If you hire even one qualifying full-time employee, you must transition to a different plan. A SEP IRA scales to accommodate employees — just know that whatever percentage you contribute for yourself, you must contribute the same percentage for every eligible employee.

You want a Roth option → Toss-up (but solo 401(k) is simpler)

The solo 401(k)'s Roth option is well-established, widely available, and straightforward. The SEP IRA's Roth option is newer (available since 2023 under SECURE 2.0), less consistently offered by financial institutions, and involves some unresolved IRS guidance issues. For Roth simplicity, the solo 401(k) still wins.

You're filing taxes in February and need a prior-year deduction → SEP IRA

A SEP IRA can be opened and funded up until your tax return's due date, including extensions (October 15 for most sole proprietors). A solo 401(k) has historically required establishment by December 31 of the tax year. However, the SECURE Act now allows retroactive establishment up to the tax return due date (including extensions) for employer/profit-sharing contributions.

Additionally, under SECURE 2.0, sole proprietors with no employees can even make retroactive elective deferrals for the first plan year, up to the unextended return due date. That said, the SEP IRA remains simpler to set up quickly, and the solo 401(k)'s retroactive deferral option is limited to the first year and only available to single-member businesses with no employees. Consult a tax advisor to determine which option applies to your situation.

You're between ages 60 and 63 → Solo 401(k), emphatically

This age window is when the solo 401(k) is at its absolute most powerful. The super catch-up contribution allows up to $81,250 total in 2025 and $83,250 in 2026 — assuming income supports it. SEP IRAs have no equivalent catch-up provision.

You want to invest in alternative assets (real estate, crypto, private equity) → Solo 401(k)

A self-directed solo 401(k) allows investment in almost any asset class without triggering the Unrelated Business Income Tax (UBIT). A standard SEP IRA at a brokerage is limited to conventional investments like stocks, bonds, and mutual funds.

You want simplicity and minimal paperwork → SEP IRA

A SEP IRA is one of the easiest retirement plans to establish and maintain. There's no annual IRS filing requirement in most cases, no plan document complexity, and no fiduciary obligations. A solo 401(k) requires you to file Form 5500-EZ once plan assets exceed $250,000, and the plan setup involves more documentation.

You'd like the option to take a loan → Solo 401(k)

Solo 401(k) plans can be structured to allow participant loans. SEP IRAs cannot. A plan loan lets you borrow up to 50% of your vested balance (maximum $50,000) without paying taxes or penalties, as long as you repay on schedule.

For greater flexibility, it can also be set up to allow for distributions in the case of hardship — meaning you can take out money early if there’s an emergency without paying any penalties. This isn’t possible with an SEP IRA, where early withdrawals might result in tax penalties.

Feature | Solo 401(k) | SEP IRA |

|---|---|---|

2025 Max (under 50) | $70,000 | $70,000 |

2026 Max (under 50) | $72,000 | $72,000 |

Catch-Up (age 50–59 or 64+) | +$7,500 (2025) / +$8,000 (2026) | None |

Super Catch-Up (age 60–63) | +$11,250 (2025 & 2026) | None |

Employer Contribution Rate | ~20% net SE income (sole proprietor) or 25% of W-2 (corp) | ~20% net SE income (sole proprietor) or 25% of W-2 (corp) |

Employee Deferral | Yes — $23,500 (2025) / $24,500 (2026) | No |

Roth Option | Yes (well-established) | Yes (since 2023; not all providers offer it) |

Roth Catch-Up Mandate (2026+) | Required if W-2 wages >$145K prior year | N/A |

RMD Start Age | 73 | 73 |

Roth Account RMDs | Exempt (as of 2024) | Exempt if Roth |

Loans Permitted | Yes (if plan allows) | No |

Employees Allowed | No (spouse only) | Yes |

Setup Deadline | Dec. 31 of tax year | Tax return due date (+ extensions) |

Annual IRS Filing | Form 5500-EZ if assets >$250K | None in most cases |

Alternative Investments | Yes (real estate, crypto, etc.) | Limited to standard brokerage options |

Saver's Credit Eligible | Yes (income limits apply; credit ends after 2026) | Yes (income limits apply; credit ends after 2026) |

Can you have both a solo 401(k) and SEP IRA?

Yes, and some freelancers have good reason to. The most common scenario: you want to cover part-time employees through a SEP IRA while also taking advantage of the solo 401(k)'s Roth or loan features for yourself.

A few important rules if you hold both:

Same plan provider: If both plans are maintained under the same umbrella, combined contributions cannot exceed the annual limit ($70,000 for 2025 / $72,000 for 2026).

Different businesses: If you have two genuinely separate businesses (e.g., consulting income and a separate rental management LLC), you may be able to contribute up to the annual limit for each — a significant opportunity.

Form 5305 limitation: If you set up your SEP IRA using IRS Form 5305-SEP, you cannot simultaneously maintain a solo 401(k). The fix is simple: don't use Form 5305. It's optional, not required.

Opening both accounts with the same company

As mentioned, if the solo 401(k) and SEP IRA plans are offered by the same company, your combined contribution for both plans can’t exceed the annual contribution limit for the year.

Using IRS Form 5305

If you use a standard IRS Form 5305 to set up your SEP IRA, you can’t also set up a solo 401(k).

Luckily there’s an easy fix: literally don’t use Form 5305. The IRS form isn’t required, and you can submit your own document. Just make sure that your plan provider (meaning, probably your company) accepts the document. Otherwise, they’ll consider you ineligible.

If you’re self-employed, retirement can seem very far away. Frankly, it’s hard for me to imagine not sitting at a computer trying to choose the right word to convey the right thought. And past financial emergencies have made me a little obsessed with having ready cash available. But then I did this calculation:

If I put $10,000 a year into a retirement plan at a 7% average real rate of return, I have twice as much money when I retire than if I just left it in my checking account.

Let me repeat that: twice as much. No more counting change!

If that isn’t an argument for investing your self-employment money in a retirement plan, then I don’t know what is!

Of course, every situation is unique. So to get the best tax advice about self-employment retirement plans, download the Keeper app to get help from a tax expert or contact Keeper at support@keepertax.com to get your questions answered today.

Read next

Neeraja Viswanathan is an attorney and freelance writer who specializes in writing about apps that help small businesses with their marketing, accounting, and tax issues. In her free time, she rides horses, reads too many novels, and writes about film adaptations on www.mysteryonscreen.com

View full bio