Filing Taxes After Divorce or Separation: Dependents, Alimony & More

Filing taxes after your divorce is stressful, but it can’t be avoided. Here's how to deal with it as painlessly as possible!

Sarah York, EASarah is an Enrolled Agent with the IRS and a former staff writer at Keeper. In 2022, she was named one of CPA Practice Advisor’s 20 Under 40 Top Influencers in the field of accounting. Her work has been featured in Business Insider, Money Under 30, Best Life, GOBankingRates, and Shopify. Sarah has spent nearly a decade in public accounting and has extensive experience offering strategic tax planning at the state and federal level. Her clients have come from a wide range of industries, including oil and gas, manufacturing, real estate, wholesale and retail, finance, and ecommerce, and she has handled tax returns for C corps, S corps, partnerships, nonprofits, and sole proprietorships. In her spare time, she is a devoted cat mom and enjoys hiking, painting, and overwatering her houseplants.

Sarah York, EASarah is an Enrolled Agent with the IRS and a former staff writer at Keeper. In 2022, she was named one of CPA Practice Advisor’s 20 Under 40 Top Influencers in the field of accounting. Her work has been featured in Business Insider, Money Under 30, Best Life, GOBankingRates, and Shopify. Sarah has spent nearly a decade in public accounting and has extensive experience offering strategic tax planning at the state and federal level. Her clients have come from a wide range of industries, including oil and gas, manufacturing, real estate, wholesale and retail, finance, and ecommerce, and she has handled tax returns for C corps, S corps, partnerships, nonprofits, and sole proprietorships. In her spare time, she is a devoted cat mom and enjoys hiking, painting, and overwatering her houseplants. Reviewed byKrislyn ChanKrislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces.

Reviewed byKrislyn ChanKrislyn is Chief Growth Officer at Keeper. At Keeper, she strives to make expert-level tax strategies that used to require a traditional CPA accessible to all. Prior to Keeper, she was at Curology, where she helped bring custom, prescription-grade skincare out of the dermatologist's office to millions of faces.

Have you ever heard of the seven year itch? No, it's not just a Marilyn Monroe movie. The phrase refers to the idea that marital satisfaction dips around the seven-year mark. And there's a US Census stat from a 2011 report that appears to give this theory some weight:

First marriages that ended in divorce lasted a median of eight years for men and women. The median time from marriage to separation was shorter — about seven years.

Divorce is ranked as the second most stressful life event a person can go through, just behind the death of a spouse. Anyone who's been through one won't be surprised to hear that. It can unsettle nearly every part of your life, which makes taxes the last thing you want to think about.

But filing after a divorce doesn't have to become its own crisis. Below, I'll walk through the questions I get asked most often as an enrolled agent, using the 2026 numbers that apply to the return you'll file in early 2027.

What should your filing status be?

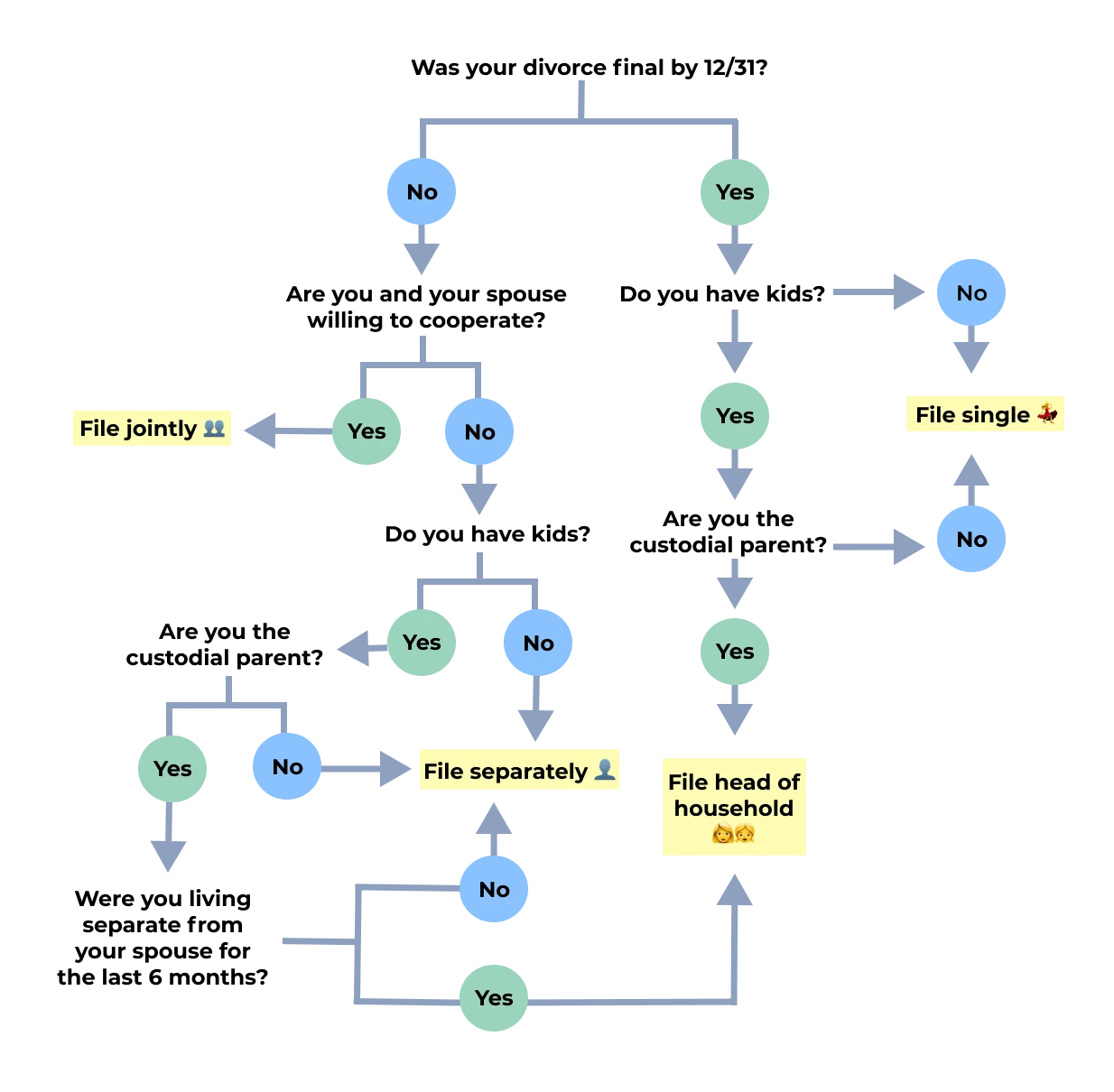

Your filing status is the first thing to nail down, and it comes down largely to one date: was your divorce or separation final by December 31?

If it was, you're treated as unmarried for the whole year. If it wasn't (even if you separated in January and the paperwork dragged on), the IRS still considers you married.

From there, four statuses are on the table:

Married filing jointly

Married filing separately

Head of household

Single

A few questions narrow it down:

Was your divorce or separation agreement in place by December 31?

If you weren't divorced or separated by year-end, are you and your ex willing to cooperate financially?

Did you and your ex live together during the last six months of the year?

Are you the custodial parent of any children?

Here's how the answers map to a status:

Filing Status | When it applies |

|---|---|

Married filing jointly | Divorce wasn't final by year-end, and you and your ex are willing to cooperate |

Married filing separately | Divorce wasn't final by year-end, and you'd rather not coordinate |

Single | Divorce was final by year-end, and you're not the custodial parent |

Head of household | You lived apart for the last six months of the year, and you're the custodial parent |

Filing jointly or single is straightforward. The two that trip people up are filing separately and head of household, so let's dig into those.

Married filing separately

This is the most common status for couples mid-divorce. Even without kids or shared assets, coordinating a joint return with an ex is often more than people want to deal with - so they file apart.

There are trade-offs, though.

You lose access to several tax breaks. Filing separately disqualifies you from claiming, among others:

Earned income credit (EITC) — though a narrow exception now lets some separated spouses claim it if they lived apart for the last six months of the year

Child and dependent care credit (for most filers)

Education credits, including the American Opportunity and Lifetime Learning Credits

And if you lived with your ex at any point during the last six months of the year, the child and dependent care credit and the adoption credit come off the table too.

The standard deduction gets complicated. For 2026, married filing separately gives you a standard deduction of $16,100. BUT you can't take the standard deduction if your spouse itemizes, and vice versa. You both have to use the same method.

The logic is that while you were living together, you likely shared expenses like mortgage interest, property taxes, and charitable giving. If one of you itemized all of those shared costs while the other took the standard deduction, you'd collectively deduct more than you're entitled to. So the IRS makes you match.

If you do itemize, you'll generally split shared expenses 50/50. In practice, most divorcing couples find it simpler to both take the standard deduction rather than coordinate a line-by-line split — even if it means leaving a little on the table.

Over 1M Americans trust Keeper for their complex taxes

The #1 tax app for freelancers, gig workers, and self-employed filers.

Get started freeHead of household

Head of household is the status to aim for if you have dependents. You'd get:

A $24,150 standard deduction in 2026 — about 50% larger than the $16,100 single filers get.

Wider brackets. The 22% rate doesn't kick in until your taxable income tops $67,450, versus $50,400 for single filers. More of your income is taxed at lower rates.

Full access to credits and deductions that married-filing-separately would disallow.

To claim it, you have to clear three hurdles.

Rule #1: You're divorced or lived apart for the last six months. You can file as head of household only if your divorce was final by December 31, or you lived separately from your spouse for the final six months of the year. (Side note: if you're still married but qualify, this is the one status that lets you pick a different deduction method than your spouse.)

Rule #2: You have a qualifying dependent. You can't have a household of one — you need at least one other person you support. Qualifying children include your:

Biological, adopted, step-, or foster child

Sibling, including step- and half-siblings

Descendant of any of the above (a grandchild, niece, or nephew)

A qualifying child generally has to be under 19, or under 24 if they're a full-time student. But children aren't the only option - a parent, grandparent, or other qualifying relative can also make you eligible, as long as their gross income for 2026 is under $5,300 and you provide more than half their support.

Rule #3: You're the primary caretaker. To count as the one footing the bill, you generally need to show that:

You didn't live with your ex during the last six months of the year

Your dependent lived with you for more than half the year

You paid more than half of their living expenses

Keeper pro tip: Child support and alimony your ex pays don't disqualify you. As long as you're spending money on the kids who live with you, you can still be the primary provider - what matters is that you can demonstrate it!

Who gets to claim the dependents?

This is where divorces get tense, because child-related tax benefits are some of the most valuable ones out there. The Child Tax Credit alone is worth up to $2,200 per qualifying child in 2026.

Usually this gets settled in the divorce agreement, and because exes don't always play nice at tax time, it's smart to spell out filing rights explicitly. If the agreement is silent, the default rule kicks in: the custodial parent claims the kids. (The custodial parent is the one the child lived with for the greater number of nights during the year.)

Keeper pro tip: Even when a divorce decree says one parent gets to claim a child, that parent still has to meet the IRS's actual requirements. Tax law beats the divorce agreement every time!

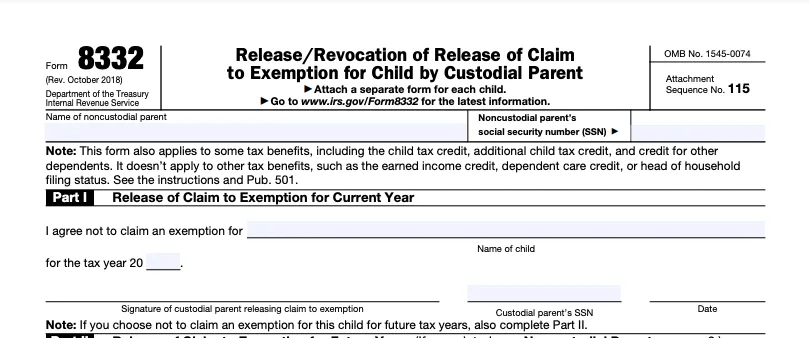

How to claim a child when you're not the custodial parent

Sometimes the agreement says the noncustodial parent should claim the child. On its own, that conflicts with IRS rules, but Form 8332 bridges the gap. It lets the custodial parent formally release the claim to the other parent. The custodial parent signs it, and the noncustodial parent attaches it to their return.

With that form attached, the noncustodial parent can claim the child even without meeting the residency test. It has to be filed for every year the noncustodial parent wants the claim, which is why a lot of co-parents simply alternate years, which is an easy way to keep things fair and civil.

What to do if your ex "revenge-files"

Revenge-filing is a real thing. Tax credits are real dollars, and an angry ex who rushes to claim your child before you do can throw a wrench in your return. When two returns claim the same Social Security number, the IRS flags it and the second return gets rejected.

It's fixable, but it's not fun. First, consider filing an extension to buy yourself time, because this takes a while. From there you have two routes:

Get your ex to amend. Ask them to file an amended return removing the dependent. It's a long shot, but if your decree gives you the right to claim the child, you can escalate to the court.

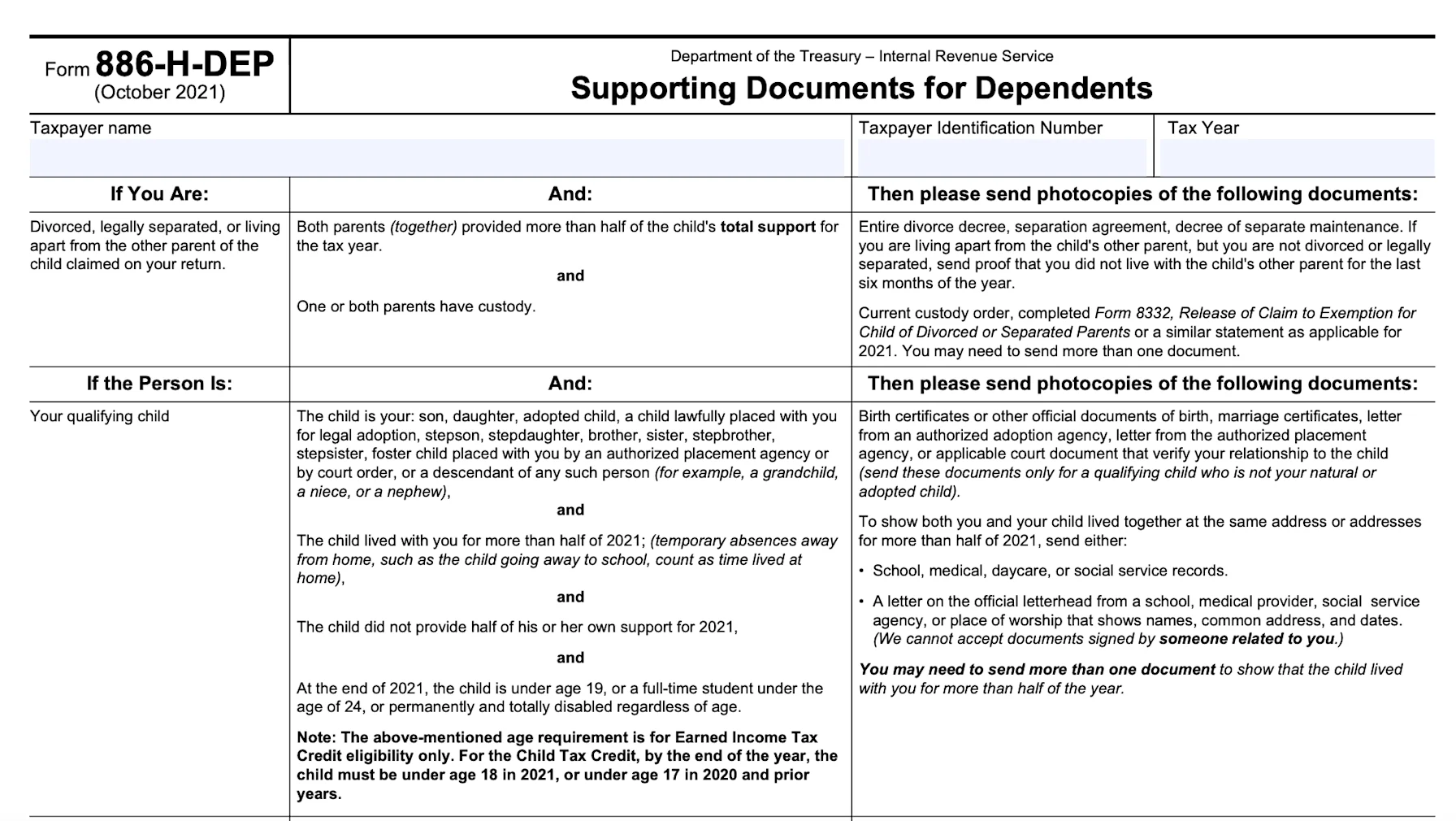

Prove you're entitled. Submit Form 886-H-DEP with documentation showing you were the one legally entitled to claim the child.

Supporting documents can include your divorce decree, the child's birth certificate, adoption papers, school or daycare records showing the child's address, and medical records. Either way, plan on six to eight weeks (sometimes longer) for the IRS to review and sort it out.

Need help sorting this mess out? Book a free call with a Keeper tax pro for more help. Your first consultation is free on the premium plan.

Do you report alimony or child support?

The rules here changed with the Tax Cuts and Jobs Act, and the confusion never really went away. The short version: it depends on the type of payment and the date of your agreement.

Child support

Do you report it? Never. Child support is never taxable to the person receiving it, and never deductible for the person paying it. It's treated as a reimbursement for shared childcare costs, so it simply doesn't appear on either return.

Alimony

Do you report it? Only if your divorce was finalized on or before December 31, 2018.

For agreements executed in 2019 or later, alimony is tax-neutral: the payer gets no deduction, and the recipient owes no tax on it. Neither of you reports it.

For agreements finalized on or before December 31, 2018, the old rules still apply - the recipient pays tax on it and the payer deducts it, so it shows up on both returns. If you modify an older agreement after 2018 and the modification explicitly adopts the new treatment, the new (tax-neutral) rules take over.

What if you changed your name when you got married?

As an accountant, this is a tradition I'd happily see fade out, because it adds a layer of paperwork at tax time. Marriages and divorces happen at the state level, and the federal government doesn't know either one occurred unless you tell it.

Submitting your name change to the SSA when you get married

If you took a new name but never updated it with the Social Security Administration, you have to file under your original name. To file under your married name, submit your marriage certificate to the SSA and get a new Social Security card. The IRS cross-checks every return against SSA records, so the names have to match.

Submitting your divorce decree to the SSA

When you divorce, if you don't want to keep filing under your ex's last name, you go through the same process in reverse - this time showing the SSA your divorce decree.

What if you shared a home with your ex?

Splitting assets is hard, and a house is the hardest of all. If you and your ex owned a home together (or live in a community property state) and it was your primary residence for two of the last five years, you can each exclude $250,000 of gain from your income when you sell. (OBBBA left this exclusion unchanged for 2026.)

But what if one of you wants to keep the house? Let's explore two common paths:

Option #1: A divorce buyout

One spouse buys out the other. Transfers of property between spouses as part of a divorce are generally tax-free, so the buyout itself doesn't trigger capital gains. The spouse who keeps the home keeps their $250,000 exclusion for when they eventually sell.

Option #2: Co-owning the home

Sometimes one spouse moves out but keeps an ownership stake. The risk: once it's no longer their primary residence, the spouse who left can lose their exclusion. The fix is to spell out the living arrangement and co-ownership in the divorce agreement. If it's clear the move was part of the settlement, the departing spouse keeps the exclusion.

What if you ran a business with your ex?

Married couples run businesses together all the time. For tax purposes, these are usually "qualified joint ventures" - the IRS treats them like sole proprietorships rather than partnerships or corporations, which keeps things simple. The one requirement is that the couple files jointly. So what happens when they split?

Option #1: Close up shop

Most of the time, the business ends with the marriage. If it holds significant assets, build the wind-down into your divorce agreement - split assets 50/50 or have one spouse buy the other out. Either way, you'll each file a final Schedule C, splitting the year's revenue and expenses 50/50.

If tracking those expenses sounds like a headache, that's exactly what the Keeper app is built for - it scans your accounts for every deductible expense and makes dividing up your Schedule Cs a lot less painful.

Track and claim every eligible deduction with Keeper

Keeper scans your accounts for write-offs and files your return — with tax pros reviewing every one.

Try it freeOption #2: File as a partnership

Once you're no longer married, you can't be a qualified joint venture anymore. To stay in business together, you'll file as a partnership using Form 1065 instead of separate Schedule Cs. Any carryover losses from the joint venture survive - you just apply them against partnership income going forward.

Like every part of a divorce, getting through tax season is easier with the right support. Keeper's team of tax assistants can help you work through these questions so you're not doing it alone. It's stressful, but with the right tools, it's absolutely doable.

FAQs

Can I file as single if my divorce isn't final yet?

No. If you're still legally married on December 31, you have to file jointly or separately - or as head of household if you qualify. You can't file single until the divorce is final by year-end.

Can both parents claim the same child?

No. Only one parent can claim a child in a given year. By default it's the custodial parent; the noncustodial parent can claim the child only if the custodial parent signs Form 8332 releasing the claim.

Is alimony taxable in 2026?

Only if your divorce was finalized on or before December 31, 2018. For agreements from 2019 onward, alimony isn't taxable to the recipient or deductible for the payer.

How much is the Child Tax Credit in 2026?

Up to $2,200 per qualifying child, with up to $1,700 of it refundable. It begins to phase out above $200,000 in income ($400,000 for joint filers).

What's the standard deduction for head of household in 2026?

$24,150, compared with $16,100 for single filers, and those married filing separately.

Read next

Sarah is an Enrolled Agent with the IRS and a former staff writer at Keeper. In 2022, she was named one of CPA Practice Advisor’s 20 Under 40 Top Influencers in the field of accounting. Her work has been featured in Business Insider, Money Under 30, Best Life, GOBankingRates, and Shopify. Sarah has spent nearly a decade in public accounting and has extensive experience offering strategic tax planning at the state and federal level. Her clients have come from a wide range of industries, including oil and gas, manufacturing, real estate, wholesale and retail, finance, and ecommerce, and she has handled tax returns for C corps, S corps, partnerships, nonprofits, and sole proprietorships. In her spare time, she is a devoted cat mom and enjoys hiking, painting, and overwatering her houseplants.

View full bio