.jpeg)

- If you miss a quarterly deadline, don't wait for the next quarter. The underpayment penalty grows the longer the balance goes unpaid, so even a partial payment now reduces what you'll owe.

- Penalties are calculated per quarter, not per year. You can pay the right total taxes for the year (or even overpay), and still get penalized for underpaying for a quarter.

- Safe harbor rules protect you from penalties. Just pay 100% of last year's tax liability (110% if your AGI is over $150K) in equal installments, and you generally won't owe a penalty, even if you earn way more this year.

- If your income is uneven throughout the year, use the annualized income installment method, so instead of making four equal payments, you pay based on. what you actually earn.

Do I need to pay quarterly estimated taxes?

Self-employed individuals will need to make quarterly estimated tax payments if they expect to owe at least $1,000 in taxes.

However, not all freelancers and independent contractors actually have to pay quarterly. If you freelance part-time or as a side hustle, you could be in the clear.

Not sure if that applies to you? Find out if you should even be worrying about estimated payments using Keeper's free quarterly estimated tax calculator.

Why are quarterly taxes required?

Long story short, the US has a pay-as-you-go tax system.

That's why employers are responsible for withholding taxes from their employees' paychecks and depositing those funds with the IRS. If you're self-employed and have enough taxable income, your quarterly payments essentially take the place of that withholding.

The payments you make four times a year will cover both your income taxes and your self-employment taxes, which W-2 employees don't have to deal with on their own. (To learn more, check out our beginner's guide to self-employment tax!)

Don't relish the idea of giving the IRS your money... let alone four times a year? Good news: You can lower your tax bill by claiming business write-offs! That's true whether you're paying quarterly or annually.

To make sure you never miss a write-off, use Keeper. Keeper is the leading tax app built to help freelancers, independent contractors, and solopreneurs automatically track their tax deductible expenses and file taxes. It automatically scans your bank accounts and helps you deduct anything you buy for work, from gas for your car to software for your laptop.

We'll help your sort out your quarterly taxes, too! Calculate how much you owe, and make payments easily.

{filing_upsell_block}

Does anyone else have to pay quarterly taxes?

Technically, self-employed people aren't the only ones who have to pay taxes in installments.

Quarterly payments also apply to other taxpayers who earn money that isn't subject to withholding. That can happen with a few different scenarios, including with:

- Business earnings

- Dividends

- Gains from the sale of assets, like stock

- Interest

- Taxable alimony

For the most part, though, estimated tax payments are associated with freelancers and business owners.

How to calculate your quarterly tax payments

Our free quarterly tax calculator is the easiest way to figure out whether you should be making estimated payments. It'll even tell you how much to set aside for each installment.

If you'd rather do the math by hand, here's how it works.

Add up how much tax you owe for the year, including both your income tax and self-employment tax. Then, divide that number by four to figure out how much you're paying per quarter.

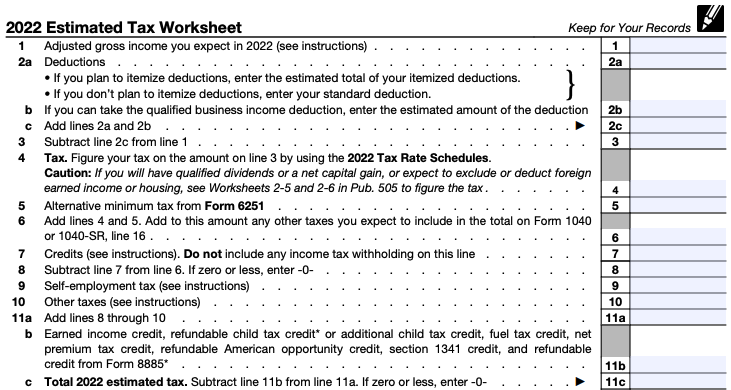

Calculating your estimated taxes with Form 1040-ES

The IRS offers a worksheet you can use to walk through the calculations. You can find it on page 8 of Form 1040-ES, "Estimated Tax for Individuals."

You don't actually have to submit this worksheet when you pay your estimated taxes.

For detailed instructions, including all your options for paying, take a look at our guide on how to file quarterly taxes!

{upsell_block}

What to do if you skipped an estimated tax payment

The IRS expects you to pay by the deadline. If you miss one, make the quarterly tax payment as soon as you can.

Some people might think, “Well, I already missed this quarterly payment. I’ll just wait until next quarter to make it up.”

Unfortunately, that could end up being a big mistake.

Why? Because the underpayment tax penalty is worked out by looking at:

- How much you you owed

- How long it took before you finally paid

In other words, you’ll pay more the longer you wait.

What if you can't pay the full amount due?

Say you know there’s an estimated tax due date coming up, but you just can't scrounge up the funds.

In that case, pay as much as you can by the deadline instead of waiting until you can pay the whole thing. Even partial payments will help reduce the penalty amounts you'll owe. We'll get into that next!

How does the tax underpayment penalty for quarterly taxes work?

The IRS estimated tax penalty isn't a flat fine. It works like interest on the amount you underpaid. The IRS divides the year into four payment periods, figures out how much you should have paid each period, and charges interest on any shortfall for the days it went unpaid.

The rate is the federal short-term rate plus 3 percentage points, which is set quarterly and compounded daily.

You can usually avoid the penalty entirely by meeting safe harbor: paying at least 90% of this year's tax or 100% of last year's (110% if your prior-year AGI was over $150,000). To learn more about safe harbor, check out our safe harbor guide or keep on reading.

Penalties include interest, which can change every quarter

What we listed above are rules of thumb that will help you get a sense of your potential penalty. But the actual penalty will fluctuate.

That's because it includes interest for missed payments, and the interest rate can change from quarter to quarter. As of Q2 2026, the interest rate sits at 6%.

Penalties are based on the quarter, not the year

It's entirely possible to pay the correct amount for the year, but still get penalized for underpayment in a specific quarter.

To take things further, you can even overpay your quarterly taxes for the year as a whole and still get penalized, as long as you were short for a quarter.

Here’s an example of this unfortunate rule at work. Say you skipped the June 15 payment, but pay extra in September to make up for it. You'll still have to pay a penalty for the estimated payment you skipped in June!

Penalties can go away thanks to safe harbor rules

Sometimes, these penalties won’t actually be enforced. Safe harbor rules can protect you from having to pay them. Here are the conditions you’ll have to meet, based on your business’s adjustable gross income (AGI):

As you can see, these safe harbor rules are based on how much you owed the previous year.

That can create some annoyances if you earn a lot more in the current year. You won't be on the hook for any penalties, but that doesn’t mean the extra is tax-free. You’ll still have to pay tax on it when you file your annual return in April, and that surprise tax bill often catches people off-guard.

Say you owed $6,000 in total tax last year. As long as you pay 100% of that, spread across your four quarterly payments, you're shielded from underpayment penalties, no matter how much more you make this year. (If your prior-year AGI was over $150,000, the target is 110% of last year's tax instead.)

But here's the catch: that's a penalty shield, not a tax discount. If your income jumps from $50,000 to $100,000, your actual tax for the year might be, say, $15,000. You avoided the penalty by paying $6,000, but you still owe the remaining ~$9,000 as a lump sum when you file in April!

Finding out how much penalty you owe

If you've been missing payment deadlines, it's surprisingly complicated to figure out how much penalty you owe. After all, a number of different factors go into this, including how much you paid, how many days you were late, and how much interest you owe.

That's why most people aren't required to figure this out by themselves. If you want to get an idea, though, you can use Keeper's estimated tax penalty calculator.

Having the IRS figure out your penalty

For most taxpayers on the hook for penalties, the IRS will calculate how much you owe.

When you file your taxes, just leave the relevant box blank on your Form 1040. (That's box 38, for "Estimated tax penalty.")

The IRS will respond by sending you a bill.

Figuring out your penalty on your own

A small number of taxpayers don't have the option of waiting for the IRS to calculate their penalty. They have to do it by themselves.

This only applies to you under three very specific circumstances:

- ✓ Your income varied a lot throughout the year, and you want to use the annualized income installment method to reduce your penalty - more on this later!

- ✓ You're applying to waive part of your penalty (as opposed to the whole thing) - more on penalty waivers below as well!

- ✓ You had tax withholding, and reporting the actual withholding dates results in a lower tax penalty than the default method of averaging it out over all four quarters.

The third one is pretty uncommon. But it could happen if your employer did something other than paying splitting your withholding into four equal chunks (like paying all of it in the first two quarters).

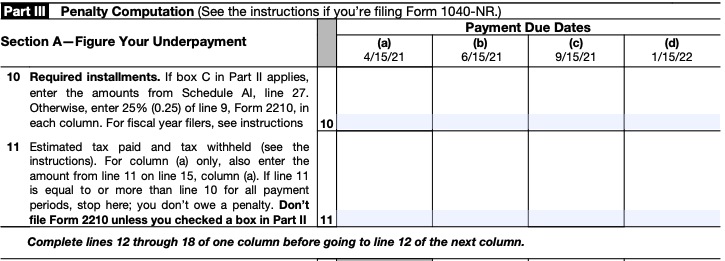

If you fall into any of those three categories, you'll have to calculate your penalty yourself. Use the worksheet on Part III of Form 2210, which is for "Underpayment of Estimated Tax by Individuals, Estates, and Trusts."

This worksheet will walk you through the whole computation. (Be sure to have your instructions on hand!)

How to get out of tax underpayment penalties

No one likes dealing with underpayment penalties. But in some cases, they're downright unfair.

Even the IRS recognizes this. That's why they've come up with a couple of ways to get out of penalties.

The first is for self-employed people with highly variable income. The second is for taxpayers dealing with special circumstances that prevented them from paying on time.

Method #1: Use the annualized income installment method if your income is uneven

People who work regular W-2 jobs can often expect the same paycheck every time. For freelancers, gig workers, and business owners, though, there's no such guarantee.

Say you run a seasonal business selling at outdoor markets when the weather's nice and closing up once winter hits. Or maybe your side gig is busiest during a particular time of year. You might even just be dealing with a rough couple of months.

If this applies to you, you can use an alternate way to calculate your quarterly estimated tax payments: the annualized income installment method.

This alternate way of calculating your quarterly tax payments lets you pay less when you earn less without underpayment penalties.

To learn more, check out our article on the annualized income installment method, which breaks down the calculations involved (with plenty of examples).

Method #2: Get your underpayment penalties waived

People with fluctuating income aren't the only taxpayers who can get out of quarterly tax penalties. As we mentioned earlier, you can also apply to waive the underpayment penalty you owe.

Many people are surprised to learn this, but the IRS is actually fairly lenient with penalties, especially if you can demonstrate you’re on top of estimated payments in the current year.

In most cases, as long as you can prove that your underpayment was the result of a “reasonable cause”, such as a family death or medical emergency, you’ll probably get a pass.

What won’t be good enough is “willful neglect” - basically, intentionally ignoring the payment.

Who qualifies for a penalty waiver

The IRS is willing to waive underpayment penalties if you:

- Became disabled

- Are at least 62 and ended up retiring

- Experienced a casualty, disaster, or other "unusual circumstance"

- Can claim the First Time Penalty Abatement Waiver

A couple of these are worth unpacking some more.

First, note that there are special rules for people who were affected by a federally recognized disaster. If that applies to you, the IRS will give you a waiver automatically - no need to file any forms.

Second, the First Time Penalty Abatement policy is for people who are either filing taxes for the first time, or dealing with their first penalty after three years without any. Basically, it’s a policy of leniency for people who aren’t very experienced with penalties.

Requesting a penalty waiver

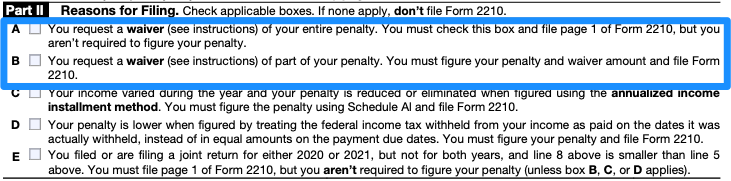

To request your waiver, fill out Form 2210 and check the right box in Part II. (It's box A for full waivers and box B for partial waivers.)

You'll submit the form along with a statement explaining why you weren't able to make your payments during the specific time period you want a waiver for.

You'll also need some documentation for your reasons. Here are some examples of the proof you might attach, depending on why you’re asking for a waiver:

Now that you’ve read this article, you’ll know what happens if you miss a quarterly estimated tax payment, and what you can do about it.

Bottom line: A skipped payment isn't the end of the world. Just make up for it as soon as you can! Your future self will thank you.

Pay your quarterly taxes accurately and on-time

Keeper Premium can help you manage and pay your quarterly taxes. No matter how complex your taxes are, Keeper can handle it.

Sign up for Tax University

Get the tax info they should have taught us in school

Track and claim every eligible deduction with Keeper

Keeper is the top-rated all-in-one business expense tracker, tax filing service, and personal accountant.

What tax write-offs can I claim?

What tax write-offs can I claim?

Discover effortless tax savings, with Keeper Tax

File complex taxes confidently

Tax Write-Offs 101: Keep More of What You Earn

Everything that freelancers, independent contractors, and new business owners need to know about deducting business expenses on your taxes, plus a live Q&A

Recommended Videos

More Articles to Read