Everything You Need to Know About Form 1099-K

Sarah York, EASarah is an Enrolled Agent with the IRS and a former staff writer at Keeper. In 2022, she was named one of CPA Practice Advisor’s 20 Under 40 Top Influencers in the field of accounting. Her work has been featured in Business Insider, Money Under 30, Best Life, GOBankingRates, and Shopify. Sarah has spent nearly a decade in public accounting and has extensive experience offering strategic tax planning at the state and federal level. Her clients have come from a wide range of industries, including oil and gas, manufacturing, real estate, wholesale and retail, finance, and ecommerce, and she has handled tax returns for C corps, S corps, partnerships, nonprofits, and sole proprietorships. In her spare time, she is a devoted cat mom and enjoys hiking, painting, and overwatering her houseplants.

Sarah York, EASarah is an Enrolled Agent with the IRS and a former staff writer at Keeper. In 2022, she was named one of CPA Practice Advisor’s 20 Under 40 Top Influencers in the field of accounting. Her work has been featured in Business Insider, Money Under 30, Best Life, GOBankingRates, and Shopify. Sarah has spent nearly a decade in public accounting and has extensive experience offering strategic tax planning at the state and federal level. Her clients have come from a wide range of industries, including oil and gas, manufacturing, real estate, wholesale and retail, finance, and ecommerce, and she has handled tax returns for C corps, S corps, partnerships, nonprofits, and sole proprietorships. In her spare time, she is a devoted cat mom and enjoys hiking, painting, and overwatering her houseplants.Form 1099-K is a tax form used to report payment card and third-party network transactions (e.g., PayPal, Venmo, eBay) for goods or services. If you made at least $20,000 on 200 transactions, you should expect to receive one!

What is Form 1099-K?

At this point, you’ve probably heard about the 1099-NEC and 1099-MISC forms. They're part of the IRS’s 1099 series. Basically, every form that starts with “1099” is going to report some category of non-W-2 income.

Form 1099-K is another hugely important form in this series. It’s issued by credit card companies and third party payment processors like Stripe, PayPal, Cash App, or Venmo. These service providers are broadly referred to as “Payment Settlement Entities” (PSEs).

The 1099-K is used to report the following types of payments to the IRS:

Credit cards (like Visa, MasterCard, American Express, and Discover)

Debit cards

Stored value cards (like gift cards)

Some work and sales platforms, like Fiverr and Poshmark, also issue 1099-Ks directly.

Who should receive a 1099-K?

Long story short, for your 2025 payments, you'll only be guaranteed to get a 1099-K if you:

Made at least $20,000 and had 200 transactions from credit cards and payment apps.

That said, some payment apps might have sent them out early even if you made a lot less thanks to an IRS rule change.

How the 1099-K rules changed again in 2022 — and then again in late 2023

If you've been paying attention to 1099 forms throughout the year, the bullet points above might look off to you. That's because the IRS keeps changing its mind.

Starting in 2022, the 1099-K was supposed to have many of the same parameters as the 1099-NEC. That originally meant getting one as long as you:

You were paid more than $600, and

You had any number of digital transactions

But the IRS decided, at the last minute, to delay putting this rule change into effect. (I really do mean "the last minute" — they sent this notice out in late December 2022.) This meant that, when taxpayers dealt with their 2022 taxes in 2023, 1099-Ks reverted to the old, pre-2022 rules.

After the 2022 delay, the change was scheduled to be implemented for the 2023 tax year. But on November 21, 2023, the IRS delayed the rule change yet again — this time citing "feedback from taxpayers, tax professionals, and payment processors" as well as an interest in "reducing taxpayer confusion."

If you're not interested in the reasoning behind this delay, skip ahead to the next section, on how 1099-Ks compare to 1099-NECs. Otherwise, stick around for some accountants' insights into the IRS drama.

For the 2025 tax year, the One Big Beautiful Bill has set the 1099-K threshold at $20,000 and more than 200 transactions.

Why did the IRS delay the $600 rule change?

There are two main reasons for the rollback:

The understaffed agency wasn't ready to roll out the change

It faced backlash from the finance agency over inconsistencies in the rules

The IRS wasn't ready

"The official answer from the IRS is that they wanted to give everyone more time to adjust to the new rules," says Meg K. Wheeler, a CPA and finance coach for small business owners. "I would also guess that they needed more time to build up their own staff in order to be able to handle the influx in paperwork they'll have to sort through."

Backlash from the industry over inconsistent rules

Jason Green, a CPA and founder of an Indiana-based tax consultancy, notes that companies pushed back in part because there's still confusion over which payment companies would be impacted — and why. Zelle, for example, is currently "exempt from the $600 rule" because "they don't hold funds, they only transfer."

"There was potential for Zelle to win a lot more business... as a result of the IRS change," Green says. "If the rules stood, freelancers looking to cheat on taxes would've likely migrated over to Zelle for payment processing."

1099-K vs. 1099-NEC: What’s the difference?

As I've mentioned, 1099-K and 1099-NEC are very similar in nature. Both can report payments made to independent contractors. So if you're a contractor, you might end up with both types of forms at tax time.

Still, there are a few important differences. And you shouldn't get a 1099-K and a 1099-NEC for the same payment. (That said, sometimes this does happen sometimes. Learn what to do about it in the section on double-reporting!)

Here are the main differences between the two forms.

1. 1099-Ks are for cards and payment apps

The main difference is the types of payments they both report. Basically, the 1099-K covers all digital transactions that aren’t ACH, EFT, or direct deposit. Those are covered by the 1099-NEC, which also covers payments by cash and check.

Here’s a simple summary of how the two forms are used:

Form | Payment Methods |

|---|---|

1099-K | Credit cards |

1099-NEC | ACT |

2. 1099-Ks cover bigger amounts — for now

For 2025 payments, a contractor has to make a lot more to be sure they'll get a 1099-K at tax time. That's $20,000, split up across at least 200 business transactions.

In comparison, to get a 1099-NEC, they'll only need to earn $600 from a client paying through ACH.

3. 1099-Ks are sent by payment processors, not individual clients

If you're a contractor, your clients are responsible for sending out your 1099-NECs. Your 1099-Ks, on the other hand, will come directly from the payment apps or credit card companies they used to pay you.

This distinction doesn't especially matter if you're only ever on the receiving end of 1099s. It doesn't matter whether your form comes from Linda, the real estate agent who hired you for some VA work, or if it's sent directly from Visa. You'll use it the same way when you file your taxes. (More on that later!)

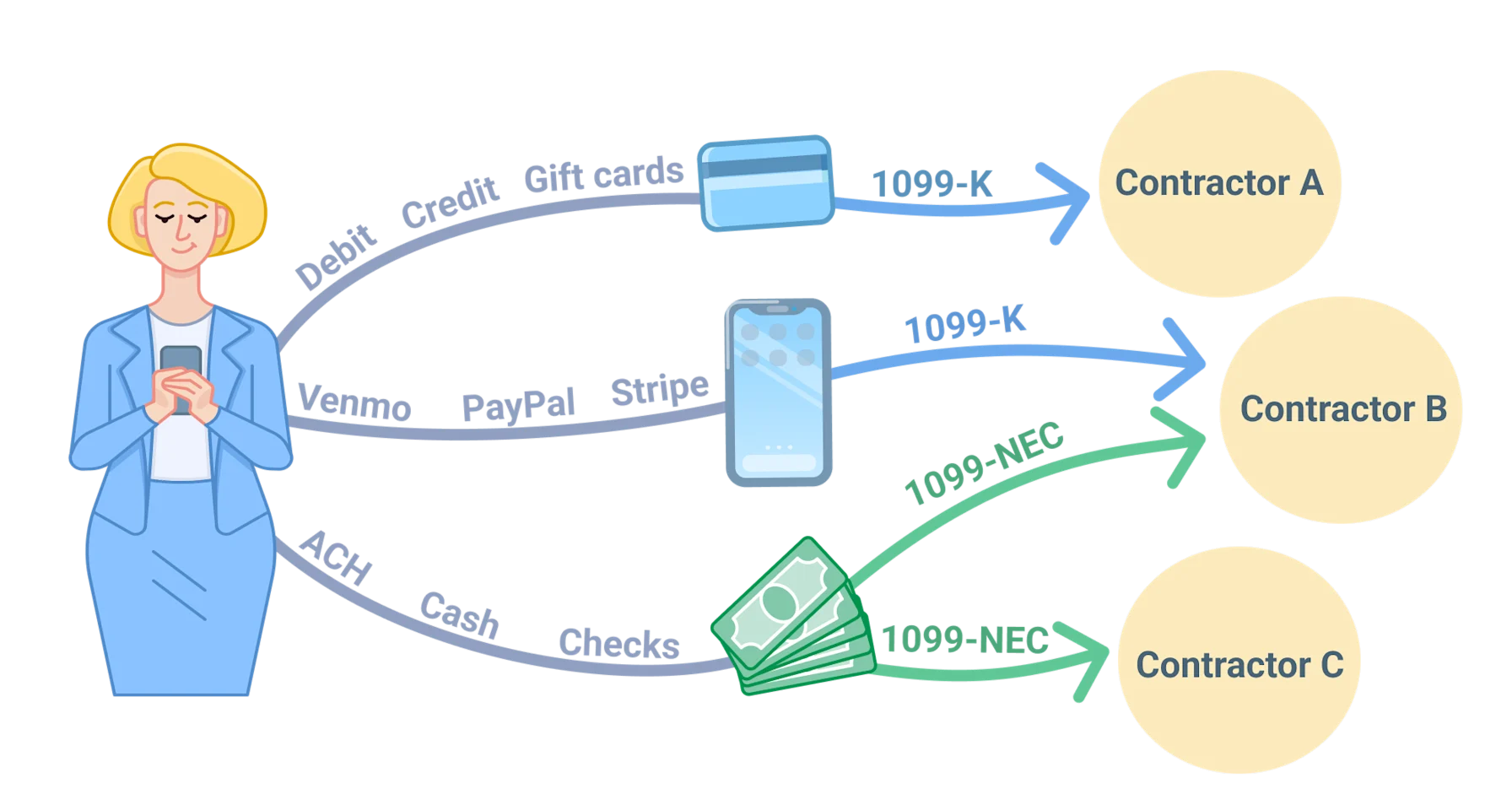

If you use contract labor yourself, though, it does matter who's responsible for issuing these forms. Say Linda paid three contractors last year, using three different payment methods.

Contractor A will receive a 1099-K, because all of their payments were made by credit card.

Contractor B will receive both a 1099-K and a 1099-NEC (depending on the amounts involved). For example, if they only received cash payments of $599, they would not need to be issued a 1099-NEC.

Contractor C will only receive a 1099-NEC, since all of their payments were cash.

"Businesses that used third-party apps like PayPal and CashApp to pay freelancers do not have to create a 1099," says Jason Green, the Indiana-based tax consultant.

Note that Zelle's unique status makes it an exception here: the IRS essentially treats Zelle payments like ACH payments. "If you pay a freelancer through Venmo or PayPal, you don't have to issue them a 1099-NEC," says Kari Brummond, a tax preparer and writer on tax-related issues. "If you pay them through Zelle [though], you do."

What to do if you get a 1099-K and 1099-NEC for the same payment

You shouldn't get two different forms for the same payment. But if you do end up with "double-reported" income, don't worry — you won't have to pay taxes on it twice.

"Be careful not to double report income when [doing your taxes] with tax prep software," says Kristine Stevenson Seale, EA, a tax resolution specialist and author.

If you get both forms, Green recommends that you "report the income listed on 1099-K alone."

"Taxpayers should keep detailed records of their income and be prepared to provide those records in the case of a dispute," he says.

Why some clients send 1099-NECs when they aren't supposed to

Not all clients realize they shouldn't be issuing 1099s for payments they made through credit card or payment apps.

"I often see business owners erroneously issuing 1099-NECs when they don't need to," says Meg Wheeler, the CPA and finance coach. This usually happens "when they have paid the person via a third-party payment tool."

This can cause headaches for freelancers. But you can address double-reporting with your own records, notes Kari Brummond, the tax preparer and writer.

"Imagine that Venmo sends you a 1099-K for $25,000," she says. "A client that paid you through Venmo sends you a 1099-K for $10,000.

"Although you only made a total of $25,000, the IRS receives two documents and believes you earned $35,000. If you file and the IRS audits your return, you need to be able to prove that those 1099s reported the same income.

"That's easy to do as long as you have the right records."

Will personal transactions show up on a 1099-K?

There’s a lot of confusion out there about this, so I want to set the record straight: the only accounts that will be issued 1099-Ks are those that are either:

Listed as business or merchant accounts, or

Personal accounts where the transactions are tagged as “goods and services,” rather than “friends and family”

That’s because personal transactions don’t count towards the 1099-K threshold. If your roommate Venmos you their half of the rent, or your aunt sends you some birthday cash via PayPal, that shouldn’t show up on a 1099-K.

What if you use the same account for business and personal transactions?

That being said, it’s extremely common for self-employed individuals to commingle their accounts – meaning, they use the same accounts for business and personal transactions.

That means if you’re using a personal PayPal account for work, the payments you receive have to be tagged as “goods and services,” or you won’t be issued a 1099-K.

If you identify as any of the following, you should probably verify that your accounts are set up correctly:

Freelancers

Gig workers

Independent contractors

Side hustlers

Members of a partnership or LLC

Anyone else with business income

What happens if you get sent a 1099-K for personal transactions?

If a payment processor sends you a 1099-K by mistake, don't worry — you still shouldn't pay taxes on that income. Here's what to do.

1. Contact the payment processor

Let them know the form they sent was inaccurate because they've counted your personal transactions.

You should find their contact info on the upper left corner of the your 1099-K. Get in touch for them and ask for a corrected form.

What happens if you can't get your form corrected? That's okay — there's a way to fix that too.

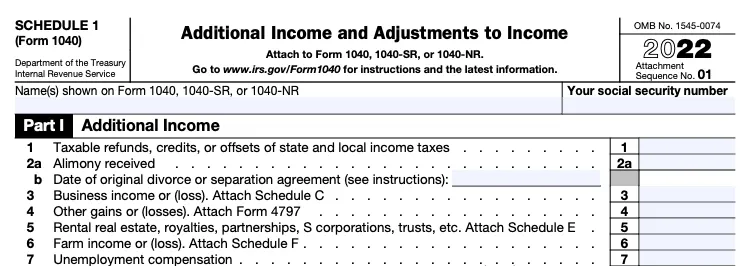

2. Deal with the error on Schedule 1 of your Form 1040

The IRS gives you a playbook for dealing with "extra" income on your 1099-K, but it's a little convoluted. You'll use Form Schedule 1. This form is used to report income from miscellaneous sources — as well as income adjustments, which are subtracted from your income.

Here's what you'll do:

Report the personal payment on Part 1 of your Schedule 1. You'll be using line 8z, for "Other Income." Put the type, put in "Form 1099-K Received in Error"

Offset it on Part II of your Schedule 1. This part of the form deals with "Adjustments to Income." You'll use Line 24z, for "Other Adjustments." Again, put in "Form 1099-K Received in Error" for the type

This basically means you add the income on one part of the form, then immediately subtract it on another part.

Here's an example. Pretend your roommate Venmoed you $700 for their half of the rent, and this got captured on your 1099-K by mistake. Here's what you'll put line 8z of your Schedule 1:

And here's what you put in line 24z:

When will you get your 1099-Ks?

Recipient copies are due January 31st, so expect them to start arriving in late January or early February at latest.

How to use the 1099-K at tax time

For freelancers and independent contractors, you’ll refer to any 1099-Ks you get when you file your taxes. The amount in box 1 of your 1099-K should be reported under gross receipts on your Schedule C.

If you’re using the Keeper app to file, you can simply upload the form and we’ll do the rest.

Over 1M Americans trust Keeper for their complex taxes

The #1 tax app for freelancers, gig workers, and self-employed filers.

Get started freeKeep in mind: The 1099-K only represents your credit card and third party payments. That means your Schedule C income might actually be higher than what’s reported on your 1099-K (after factoring in your additional income from cash and checks).

What to do if your Schedule C income is less than your 1099-K income

Occasionally, your gross receipts on Schedule C might be less than what’s reported on the 1099-K.

This could be the result of commingling your business account with your personal account, or a timing difference.

For instance, the credit card company might include a transaction that was made on 12/31, but didn’t hit your bank account until January 3rd of the following year.

If that happens to you, be sure to keep notes explaining the difference. The IRS’s database is built to flag discrepancies between 1099 forms and the corresponding tax returns. They even designed custom notice letters for taxpayers who underreported their 1099-K earnings. So if you report less than the 1099-K, keep notes!

Understanding your 1099-K

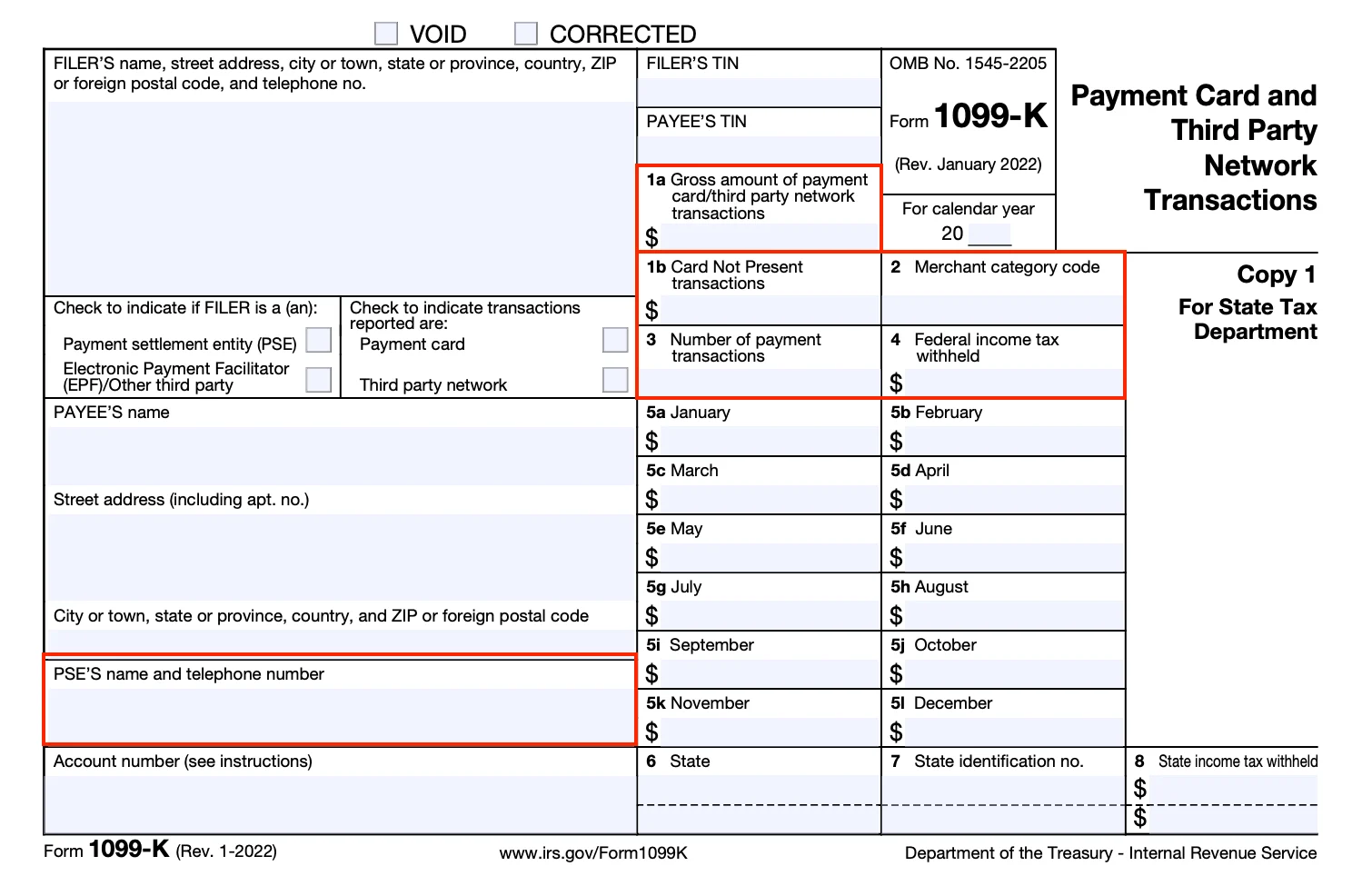

To make sure you’re reading your 1099-K correctly when it’s time to file taxes, let’s take a peek at the key boxes on this form. They’re higlighted in red on the form below, so you can follow along:

Box 1a: Gross payments

As discussed above, box 1a is what you’ll report on your Schedule C as gross receipts. This is the only box that really matters for most taxpayers.

Box 1b: Card not present

This box represents payments that were made with a credit card that wasn’t physically present — such as payments online or phone payments. In many cases, box 1a and 1b will be the same.

Box 2: Merchant category code

A merchant category code is used to describe what industry the revenue is being generated in.

You don’t need to do anything with it, but it’s worthwhile to make sure it’s consistent with the NAICS code you pick for your Schedule C.

For instance, if you work in ecommerce, and the code on your 1099-K is 5812 - “Eating Places and Restaurants,” you should probably reach out to the 1099-K issuer and request a more accurate code.

Box 3: Number of payment transactions

This is a relic of the old 1099-K rules that required at least 200 transactions before the reporting requirement kicked in. All this shows is the number of transactions that occurred during the year.

Box 4: Federal withholding

Not many recipients are going to have federal or state withholding, but if you do, don’t miss it! Always be sure to report the withholding on box 4 or 8 on your 1040 return.

Box 5a-i: Monthly transactions

These boxes are informational and don’t typically have any application on your return.

PSE’s name and telephone number

The last box I want to call out is the contact info for the Payment Settlement Entity (PSE). If you notice a mistake on your 1099-K, this is the number you should call to correct the error.

What to do if your 1099-K is wrong

There could be a number of reasons why your 1099-K is incorrect, but let’s take a look at the most common – and what to do about each of them:

Information errors on your account

If your online account lists the wrong business name or tax ID number (SSN, EIN, or ITIN), your 1099-K will probably need to be corrected.

Reach out to the payment settlement entity listed on your form to have this information updated.

Personal account used for business

This is extremely common: many freelancers end up using their personal accounts for work and forget to have their customers tag payments as "goods and services." Consequently, the merchant doesn’t issue a 1099-K for their income.

If this happened to you, don’t fret! Simply report the business income that was made through your personal account last year, and get set up with a business account for all future payments. No need to contact your PSE and request a 1099-K.

Shared credit card terminal

In some instances, multiple people or businesses will share the same credit card terminal or merchant account. In those cases, inform the PSE which payments apply to your business so that your sales aren’t overstated.

Entity change

If your business entity changes during the year or you register for a new tax ID number or business name, the PSE will need to be informed.

Cashback payments

If you allow customers to get cash back using their debit card, it’s likely those will be reported on your 1099-K even though they aren’t revenue to you.

If that’s the case, you have two options. You can either:

Contact the PSE and request a corrected 1099-K, or

Report the cashback payments on your Schedule C under “Other expenses” or “Returns and allowances” to offset the overstated income.

General guidance for all 1099 forms: They should support the records you already have, not be relied upon to create them. Best practice is to keep track of your business income and expenses throughout the year, and use the 1099s you receive as additional verification.

The Keeper app can help streamline this process for you by tracking and sorting your business expenses as you go.

Track and claim every eligible deduction with Keeper

Keeper scans your accounts for write-offs and files your return — with tax pros reviewing every one.

Try it free